Macroeconomics Notes for Oxford PPE Finals

Wed Mar 31 2021tags: notes ppe oxford macroeconomics economics finals

Introduction

These are notes I (Lieu Zheng Hong) wrote for myself while preparing for my Oxford PPE Finals. Some of my juniors asked for my notes and I am happy to oblige.

I provide these notes free to all but I ask that you do not reproduce them without first obtaining my express permission.

There are lots of mistakes, omissions, and inadequacies in these notes. I'd love your input to help make these notes better, by emailing me or by sending in a pull request at the GitHub repo here.

- Download the PDF here.

- TODO: autogenerate PDF using a GitHub action after every merged PR.

Table of contents

Key equations in all the models

IS-PC-MR model

From Celine (rework):

We assume a closed economy with imperfect competition on the supply side and flexible wages and prices, which can be set according to the trade unions' and firms' objectives respectively. Further, we assume an inflation targeting CB with a static loss function and adaptive expectations of private sector agents. The IS curve captures the negative correlation between interest rates and output, as higher interest rates dampen investments and hence decrease output. There is a one period transmission lag. The positive correlation between output and inflation is denoted by the Phillips curve (PC). The PC is upward sloping, because away from equilibrium, demands of higher wages lead to increases in inflation as firms have a last mover advantage.

The steepness of the PC is determined by the relative slopes of the WS and PS curves - this captures how aggressive the wage-price mechanism between firms and worker unions is. The Monetary Rule (MR) shows the CB’s set of best responses, that is, the “optimal” trade-off between inflation and output. It is obtained by minimizing the CB’s convex loss function subject to the PC constraint.

Static loss function:

Dynamic loss function:

NKPC

where and is the proportion of firms who get to set prices costlessly.

There is also an equivalent formulation of the NKPC:

REPC

Interpretation: inflation today is formed by expectations of all information from the past that is available. means expectation of from all information available at the end of period .

Long-term interest rates

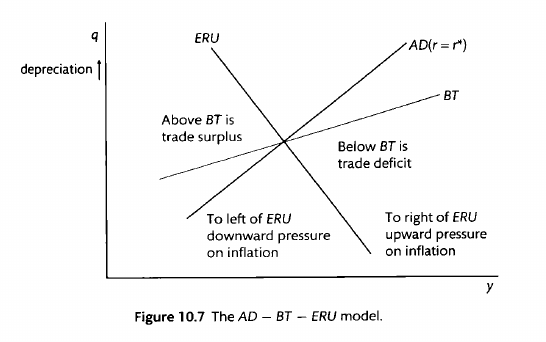

Open economy model

The AD curve is defined as the output-exchange rate tradeoff in the MRE. It combines the IS and the UIP to get a relationship between the real exhcange rate and output. We cannot be off the AD curve. The AD is the medium-run equilibrium. No time subscripts

Solow growth model

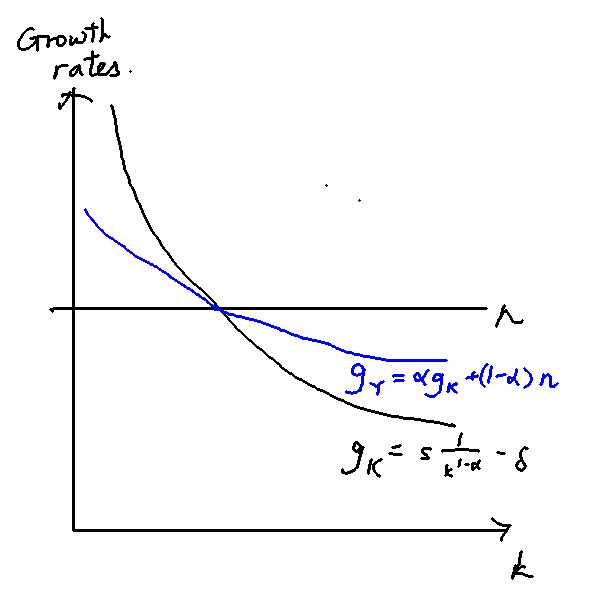

Growth rate of capital and output

which tells us that the growth of the capital stock actually decreases with per-capita capital. Because , decreases as increases. This makes sense precisely because of diminishing returns. The more capital you have, the slower capital grows. Finally, let's look at the growth rate of output, . We start with the Cobb-Douglas production function (letting A =1 for simplicity), take logs, and differentiate to get:

The expression is easily understood. The growth of output is a weighted sum of the growth of capital and the growth of the labour force, with weights equal to each factor of production's contribution to the production function.

Harrod-Domar formula

Fundamental Solow Equation of Motion

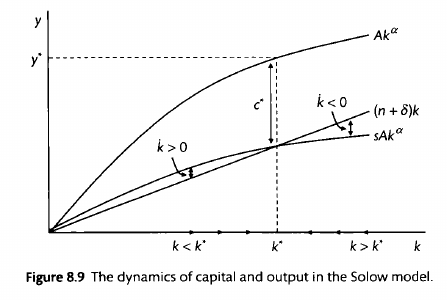

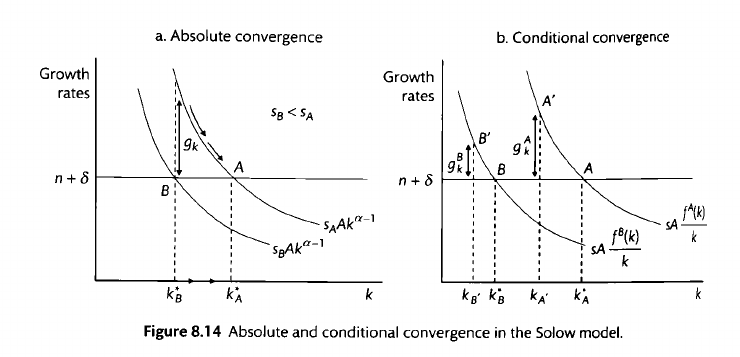

Steady-state values of capital and output under the Solow model

We know that at the steady state, the ratio of capital to labour does not change: that is: . With this, and the Fundamental Solow Equation of Motion, we have:

Given that , we can also solve for , to obtain:

Romer and Jones

Romer:

Jones:

Derivation of growth rates of capita and output

We know that and thus .

Take logs of both sides of and differentiating with respect to time gives us

Multiply both sides of the equation by :

Given that , and in the steady-state BGP the growth of the growth rate , we divide both sides by to get:

Rearrange to get the desired expression:

The second equation is just the result above multiplied by :

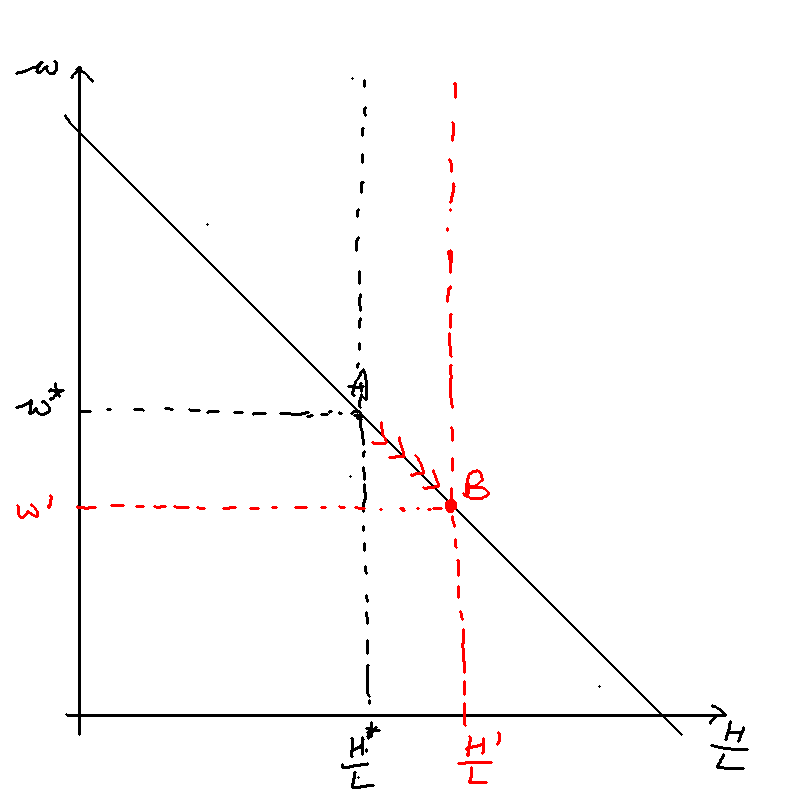

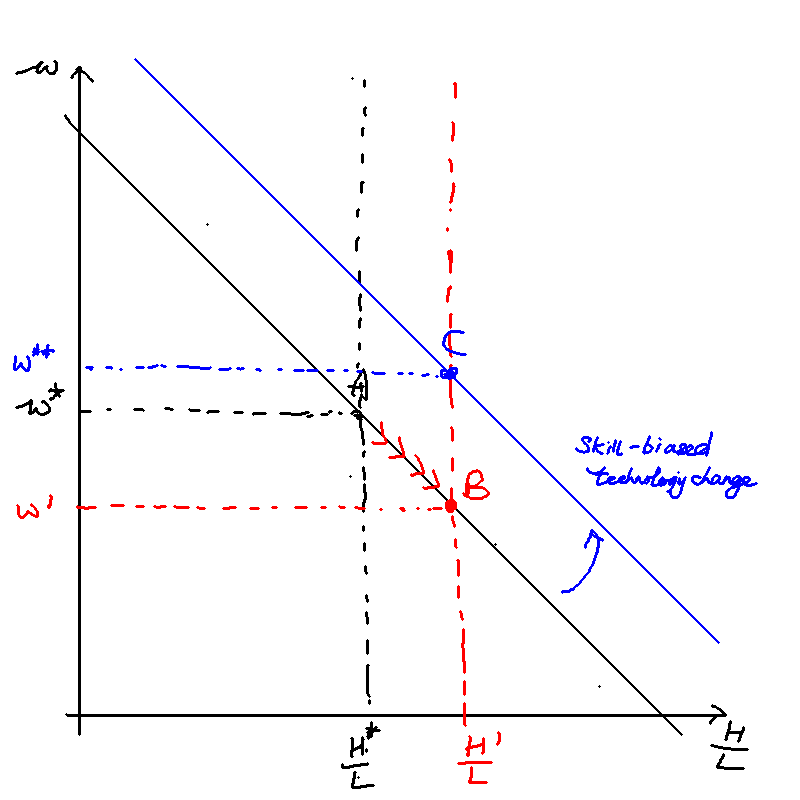

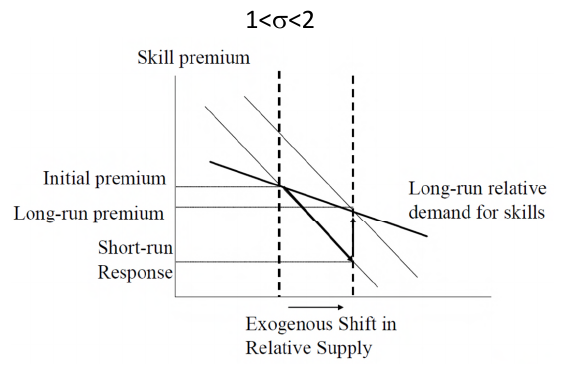

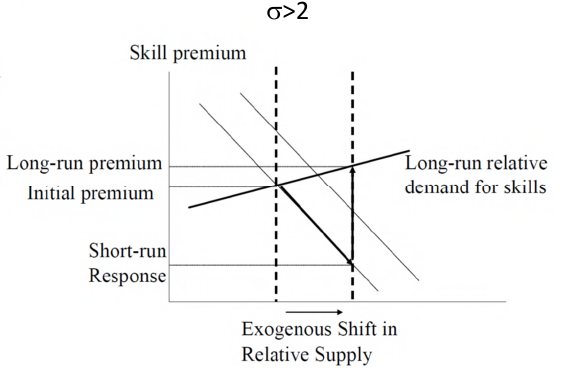

Acemoglu's directed technological change

As this is a competitive labour market, the wages of high- and low- skilled workers must equal their marginal productivities and . Some algebra gives us the following:

The skill premium, , is given by the ratio of to . After taking logarithms on both sides, we obtain

where is the elasticity of substitution:

This gives us

This gives the result that when , more technology will be produced for the higher-skilled worker if H/L increases (i.e. the market size effect dominates). This is something we previously assumed in the exogenous case, but now we have derived it.

We've shown that if , more technology will be produced for the higher-skilled worker if increases. But what about the skill premium? The relative wages of skilled workers (the skill premium) will increase if . The skill premium can be obtained as follows:

\begin{equation} \omega \equiv \frac{w_H}{w_L} = \left(\frac{A_H}{A_L}\right)^\rho \left(\frac{H}{L}\right)^{-(1-\rho)} \end{equation}

Substituting the result we got for into the equation, as well as the fact that , we obtain

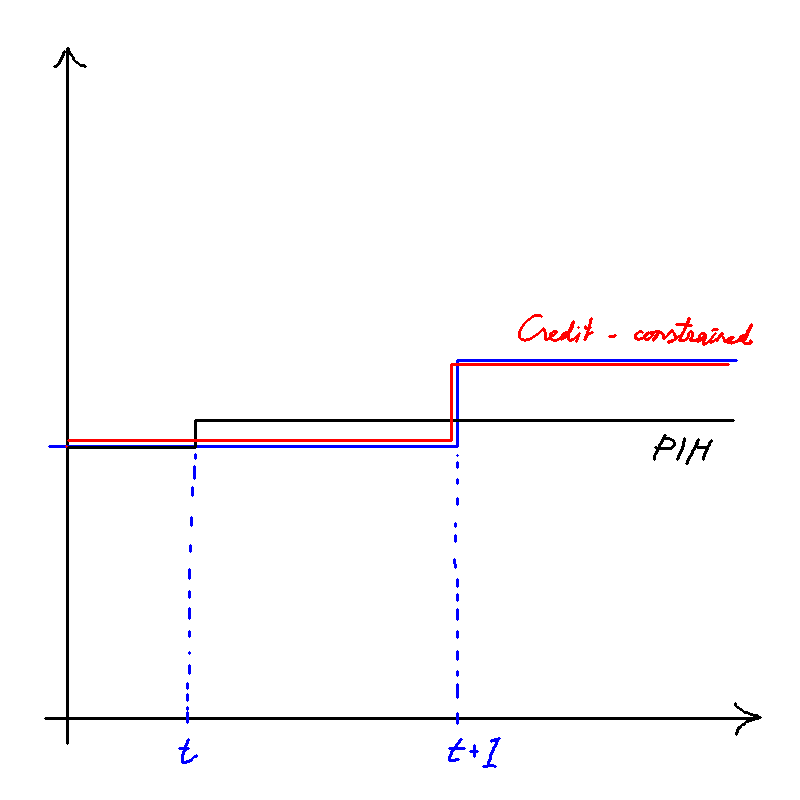

Intertemporal consumption

The interpretation of this budget constraint is that the expected total future consumption (LHS) must be equal to the total expected income plus whatever initial endowment the household had in the beginning (). This is called the present value (PV) constraint.

Euler equation

The household maximises expected utility subject to the PV constraint. It can be shown that the first order conditions imply that for any ,

This is the Euler equation.

PIH

which holds for all values of t. That means that MU is expected to be constant (assuming that )

Hall's random walk model

RBC

In the RBC model, we assume a simple Cobb-Douglas production function that depends on both labour and capital. We use a Solow-Swan growth model to endogenise the savings rate, explaining how and why households save: because they get the marginal productivity of capital.

The production function is given by

We assume perfect factor markets. Profit maximisation by firms means that wages and interest rates equal the marginal products of labour and capital respectively:

Importantly, We can see that and depend positively on , but increases with the ratio while decreases.

The Cobb-Douglas production function has constant returns to scale.

Households optimally allocate time between labour and leisure, and trade-off consumption and saving. All savings are invested and become capital in the next period. Households maximise their intertemporal utility function

Households' savings accumulate as capital according to the following capital accumulation equation:

There are three key equations:

- the consumption Euler equation (trading off consumption now v. consumption later),

- the intratemporal labour supply equation (trading off labour and consumption within a singular period), and

- the intertemporal labour supply Euler equation (trading off working now v. working later)

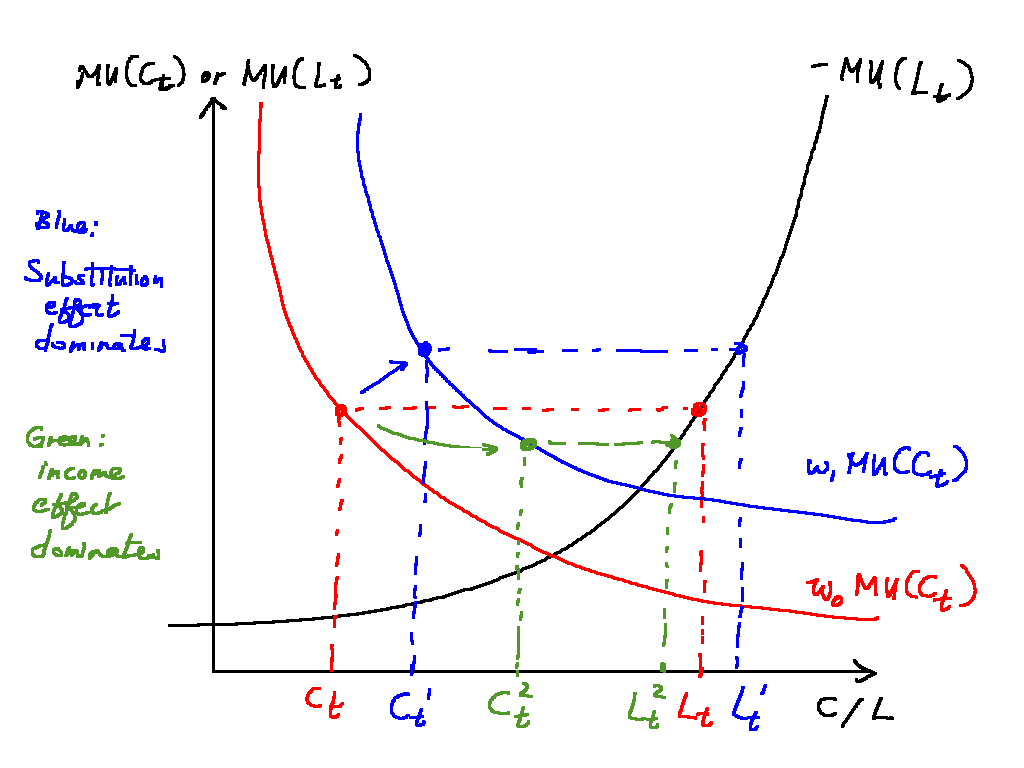

One key assumption is that a permanent increase in the real wage (such as the one associated with technical progress) generates exactly offsetting income and substitution effects such that labour and leisure are left unchanged. This is meant to match the empirical fact that despite increased labour productivity, hours worked have not changed in many decades.

An implication of this is that labour supply will rise in response to a temporary productivity increase, since the income effect is much smaller with a temporary shock.

\pagebreak

The IS-PC-MR model

Microfoundations of the PC curve

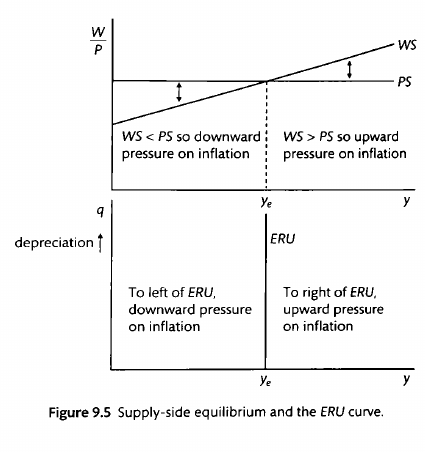

WS-PS model

The IS-PC-MR model

Substituting the IS curve into the MR curve gives

where is the economy's sensitivity to interest rate changes, is the slope of the Philips Curve, and is the central bank's inflation aversion.

Determinants of the PC

The slope of the PC is determined straightforwardly by the slopes of the WS and PS curves. The slopes of the WS and PS curves are themselves determined by marginal productivity of labour, bargaining power/monopsony power, etc.

Determinants of the MR curve

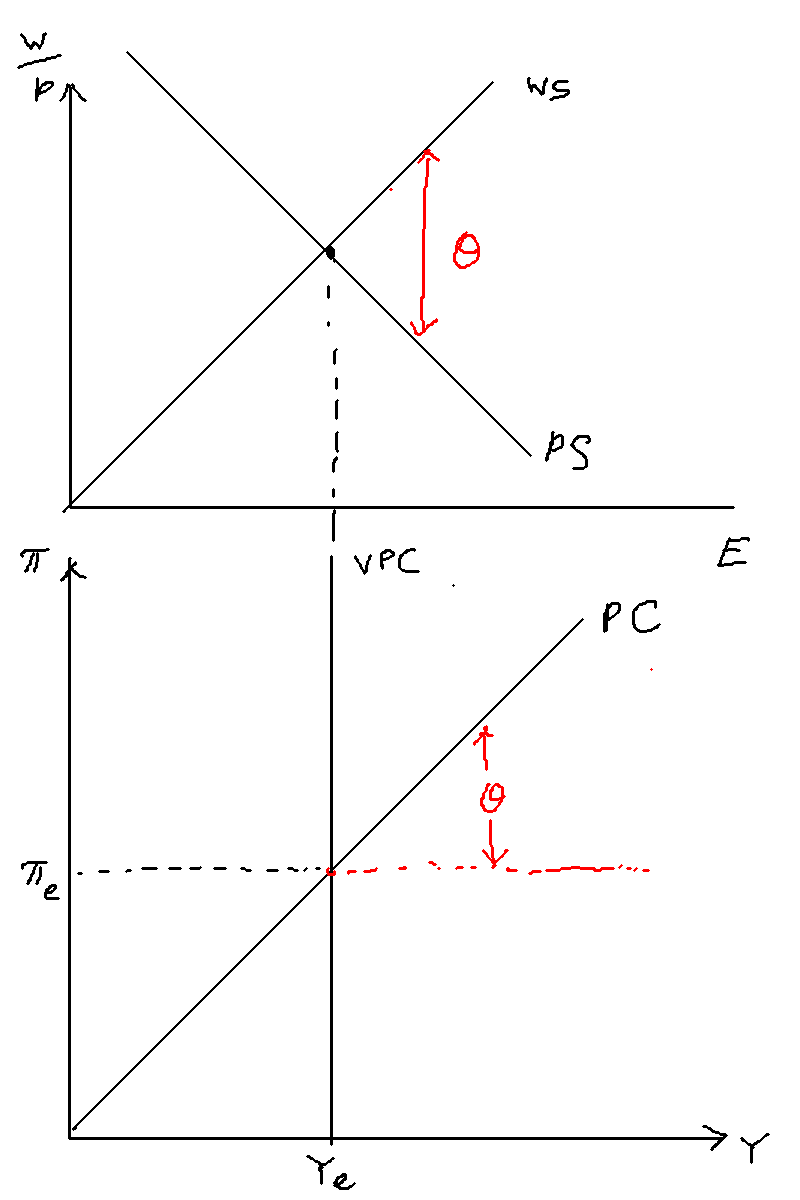

The slope of the MR curve is determined by the , and the coefficient.

The effect of and are straightforward. A greater makes the central bank more risk-averse and thus flattens the MR curve: the central bank is willing to trade off more output in order to control inflation. A greater

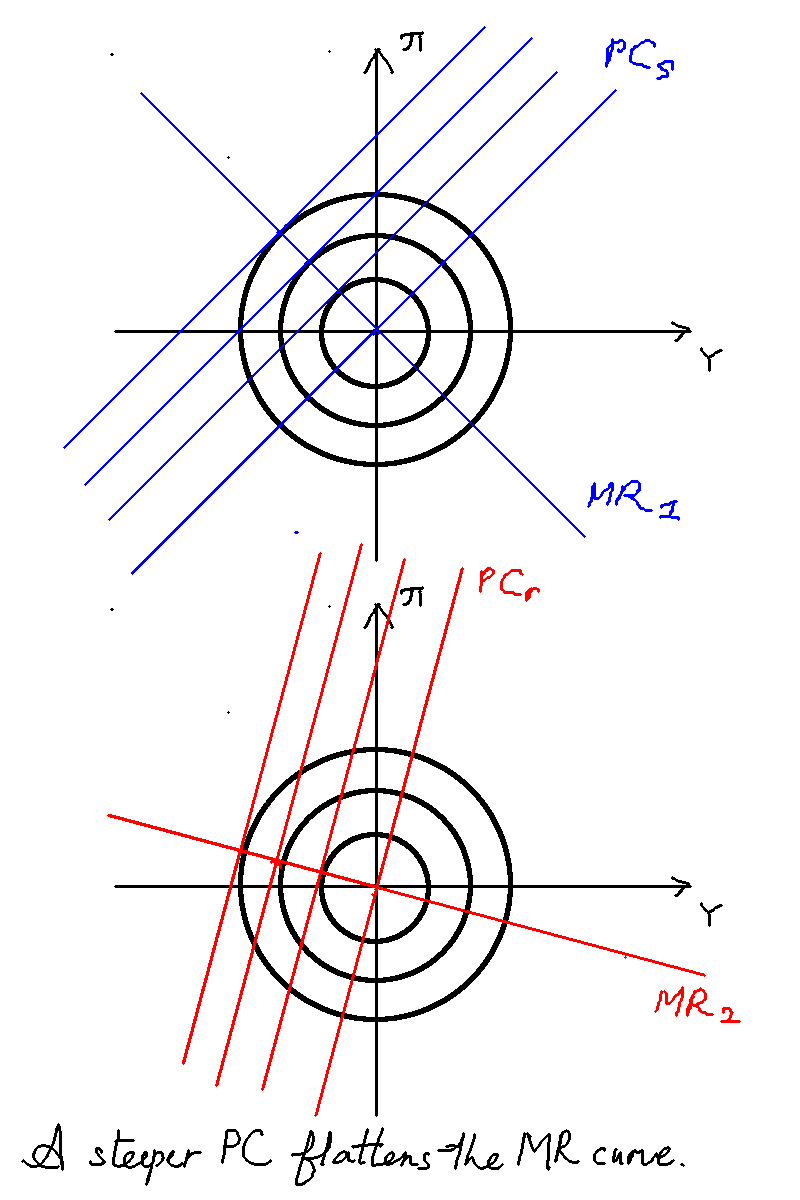

The effect of is ambiguous, however. It's basically identical to the contrained optimisation problem of labour and leisure. As increases (denoting a steeper PC), monetary policy is more effective, and it's easier for the central bank to control inflation, so it needs to do less of it.

At the same time, however, a steeper PC flattens the MR curve, and so the bank is more willing to do more. (Substitution effect).

The overall effect is similar to a worker trading off labour and leisure, and the wage rate increasing. By the income effect, the worker can afford to work less, but at the same time, the substitution effect means the worker wants to work more.

In Chris Bowdler slides, he takes the partial derivative of and finds that the first effect dominates iff when . That is to say, an increase in causes a decrease in the central bank's chosen inflation reduction when .

With what we know now, we can easily answer this PYP question:

2014 Part A: Suppose that at low levels of inflation, the coefficient on the output gap in the Phillips curve decreases in size. If monetary policy makers care equally about the output gap and inflation, what are the implications for the monetary rule curve?

This is basically saying that increases as the gap increases. What are the implications? Well, as we mentioned, the flatter Philips Curve could have two effects: it makes monetary policy less effective, which means the central bank wants to do more and less of it. Which effect dominates depends on . The larger is, the more likely that the central bank will want to do more.

Types of different shocks

-

Demand shock

-

Cost-push shock

-

Productivity shock

-

Bargaining power shock

-

Unobserved/observed? One period, two periods, permanent?

-

Under AE? RE? Static or dynamic loss function?

We note that central banks can always react immediately, but changes in interest rates need one period to take effect.

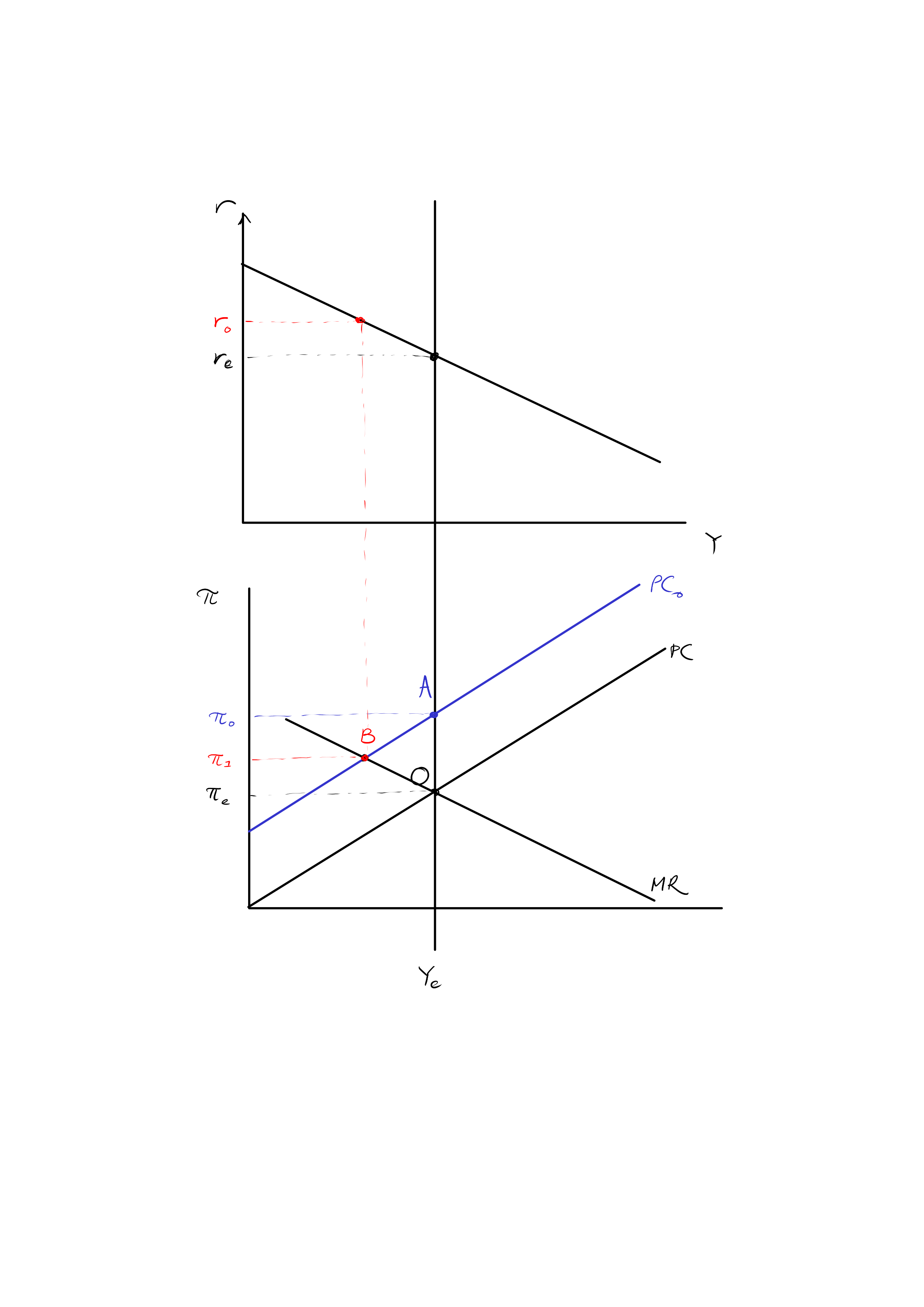

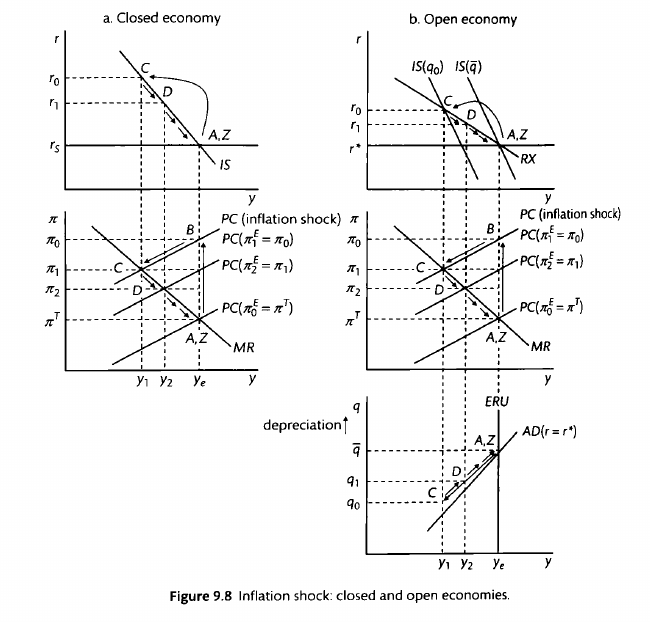

A one-period positive demand shock

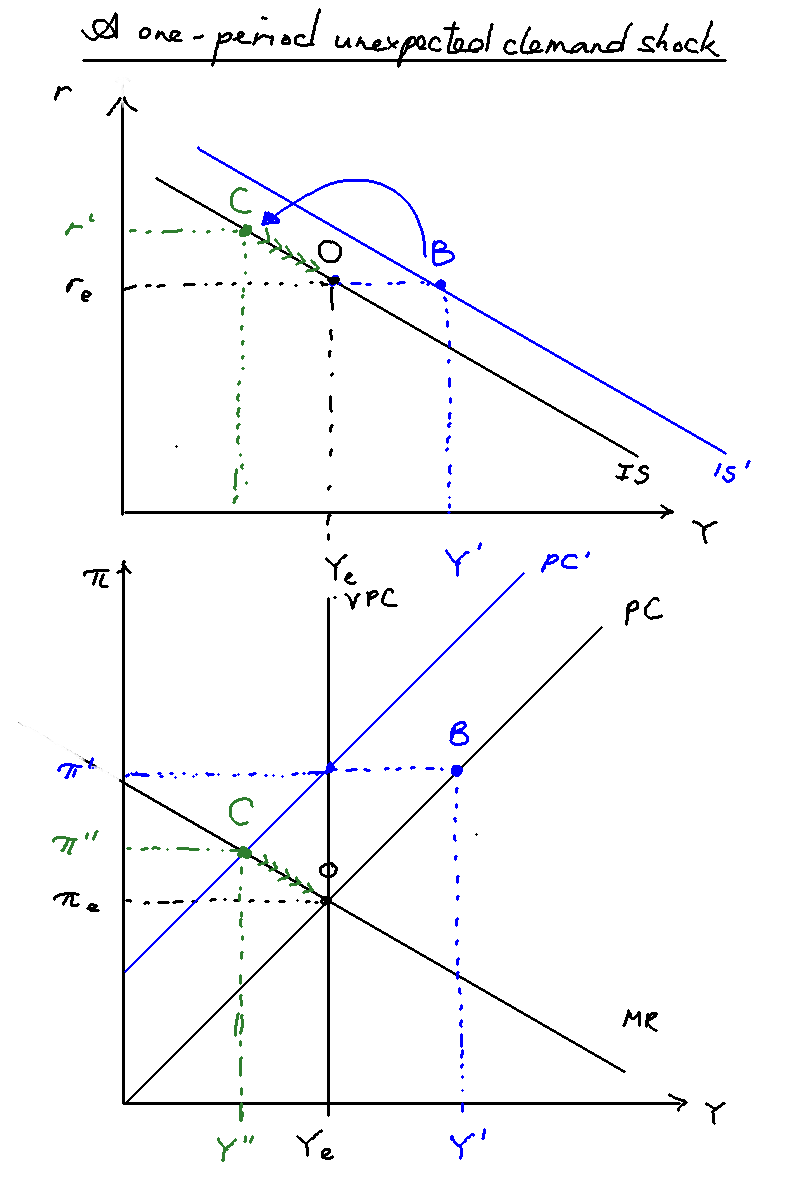

Consider the simplest possible shock: a one-period unexpected positive demand shock under adaptive expectations and a static loss function. What happens? This happens all the time, and it can be quite tricky. The key is to be very clear about what happens when. I find it helpful to think of the central bank as acting between periods, like a "end-of-turn" effect.

t=0: We start at O, the equilibrium. There is an unexpected demand shock that causes the IS curve to shift to the right, from O to B. This causes inflation and output to also move from equilibria of to and to (in blue).

t=0: Upon observing the shock, the central bank responds immediately. It needs to hike rates. But what rate should it choose? Knowing that inflation expectations will rise next period from to (blue), it chooses a rate that is its best response to that PC --- the intersection of and MR. Working under the assumption that the shock is temporary, and the IS curve will go back to normal next period, it thus hikes rates to to reach point C on the old IS curve (in green). But there is no effect of output due to the one period lag of policy transmission.

t=1: The rates take effect. As mentioned, the PC shifts up due to heightened inflation, and due to the bank's heightened interest rates the output drops from to . We are now at point C.

t=2 onward: We slowly move back to equilibrium. The bank slowly reduces interest rates and the PC slowly falls until we are back at point O.

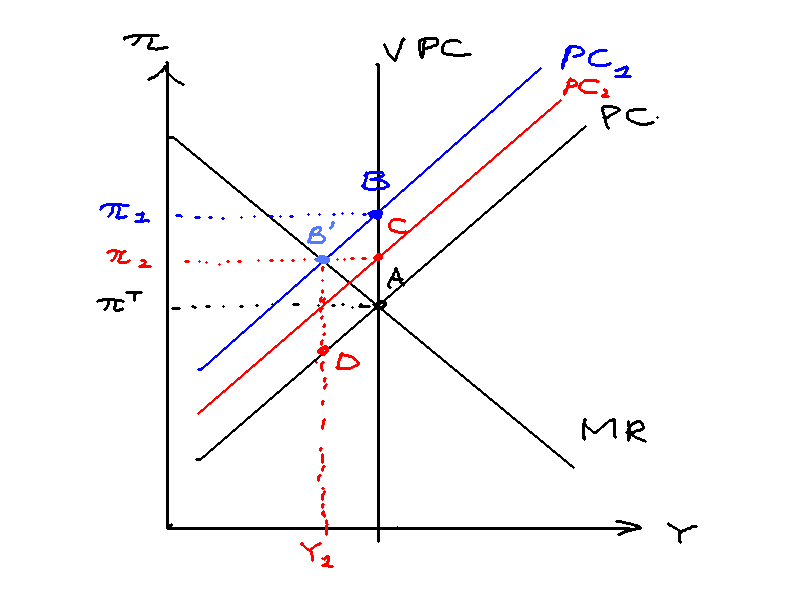

A two-period positive demand shock

Now let's consider a simple extension of the one-period positive demand shock. Consider a shock that is unexpected, but upon arrival we know that it will last for exactly two periods. How does this change the analysis? Turns out, not much.

t=0: We start at O, the equilibrium. There is an unexpected demand shock that causes the IS curve to shift to the right, from O to B. This causes inflation and output to also move from equilibria of to and to (in blue).

t=0: Upon observing the shock, the central bank responds immediately. It needs to hike rates. But what rate should it choose? Knowing that inflation expectations will rise next period from to (blue), it chooses a rate that is its best response to that PC --- the intersection of and MR. In contrast with the one-period demand shock, it knows that the shock will last for another period, and so it hikes rates not to in green, but in red, to reach point C on the graph. Again, there is no effect of output due to the one period lag of policy transmission.

t=1: The rates take effect. As mentioned, the PC shifts up due to heightened inflation, and due to the bank's heightened interest rates the output drops from (blue) to (red). We are now at point C. The central bank knows that the IS curve will fall back to normal, and the PC will move from to , so it lowers rates to reach point D on the equilibrium.

t=2: We move to point D.

t=3 onward: We slowly move back to equilibrium. The bank slowly reduces interest rates and the PC slowly falls until we are back at point O.

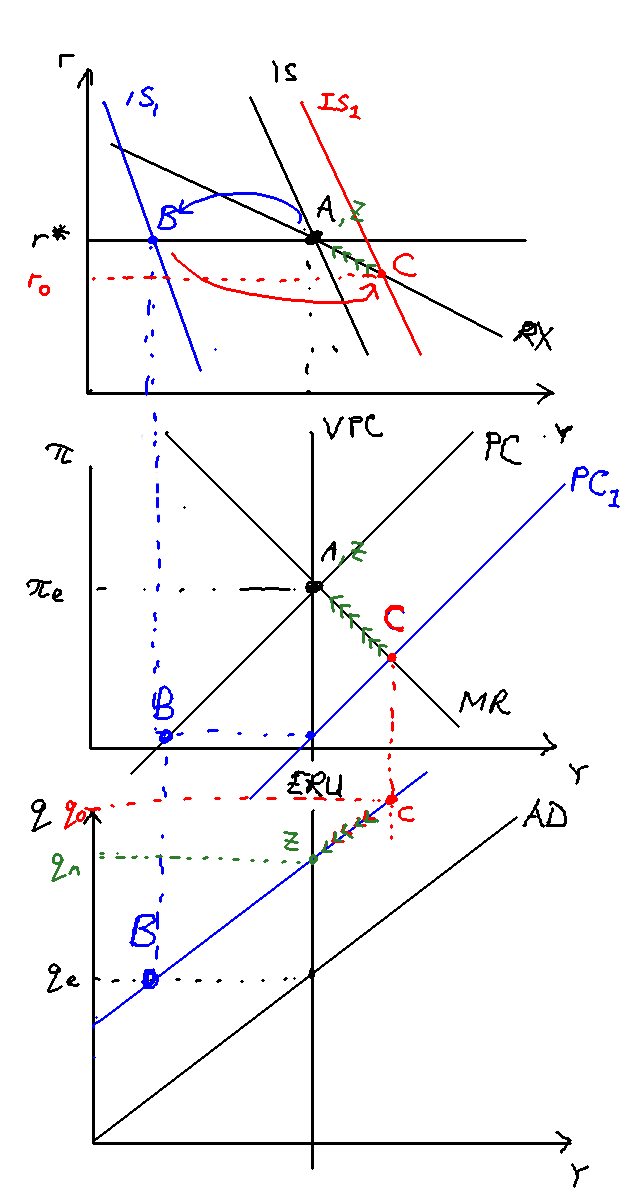

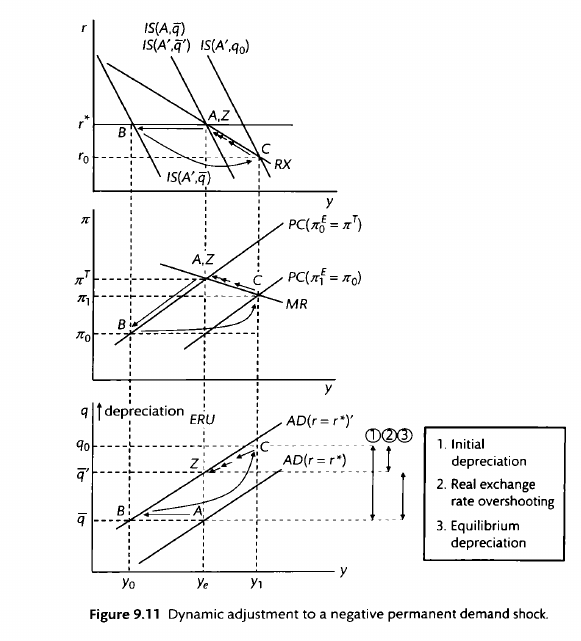

A permanent negative demand shock

Finally, let's look at a permanent fall in demand. This is actually quite easy. The IS moves permanently from to . Everything else is the same.

The key is to look at the right hand side. We can see that while interest rates fall immediately, the change isn't reflected in either output or inflation until the next period.

An unexpected one period cost-push shock

Figure \ref{one_period_cost_push} explains. The economy is initially at equilibrium, with output = on the VPC and inflation at target. This is point O on the diagram.

An unexpected one-period cost-push shock in t=0 causes the PC to shift up to , in red. Inflation rises from to . The central bank knows that the shock will dissipate in the next period, but inflation expectations will be permanently elevated, causing the PC in period to be at . It therefore raises rates to to reach point B on the MR curve (in blue). However, because of the one period lag between interest rates and output, there is no change in this period.

In period t=1, the PC remains at as predicted, and we indeed move to point B on the MR. The central bank knows that this will cause the PC in the next period to fall, and again lowers rates to reach its preferred point on the intersection of the MR and the new PC (not pictured). There is therefore a slow fall in inflation and rise in output as the economy slowly returns to equilibrium.

A permanent cost-push shock

A cost-push shock permanently moves the PC upwards, which causes the rate of inflation

Again, note that and react right away, but there is a one period lag in the output .

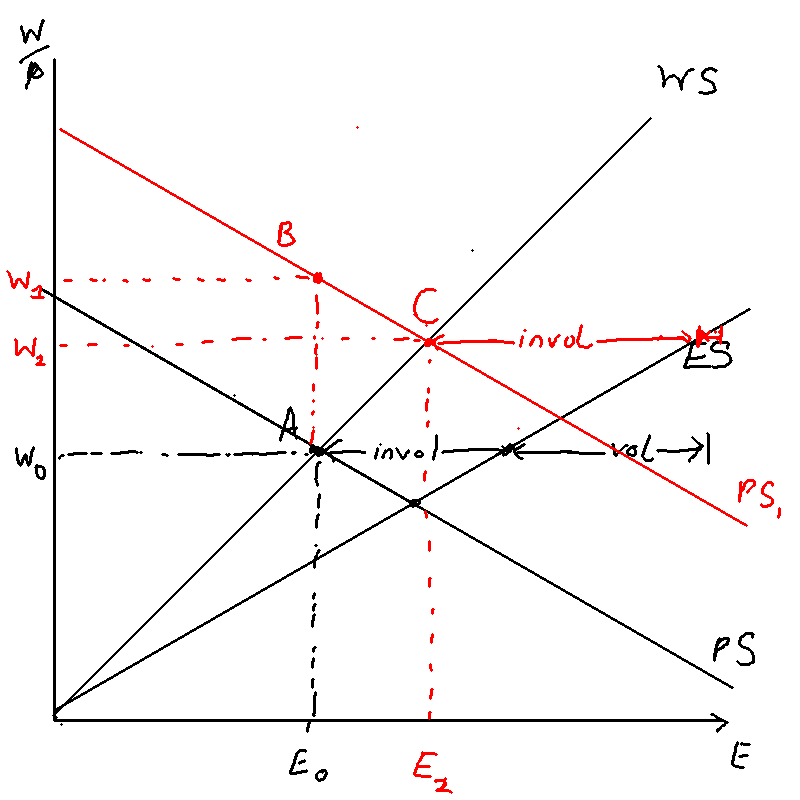

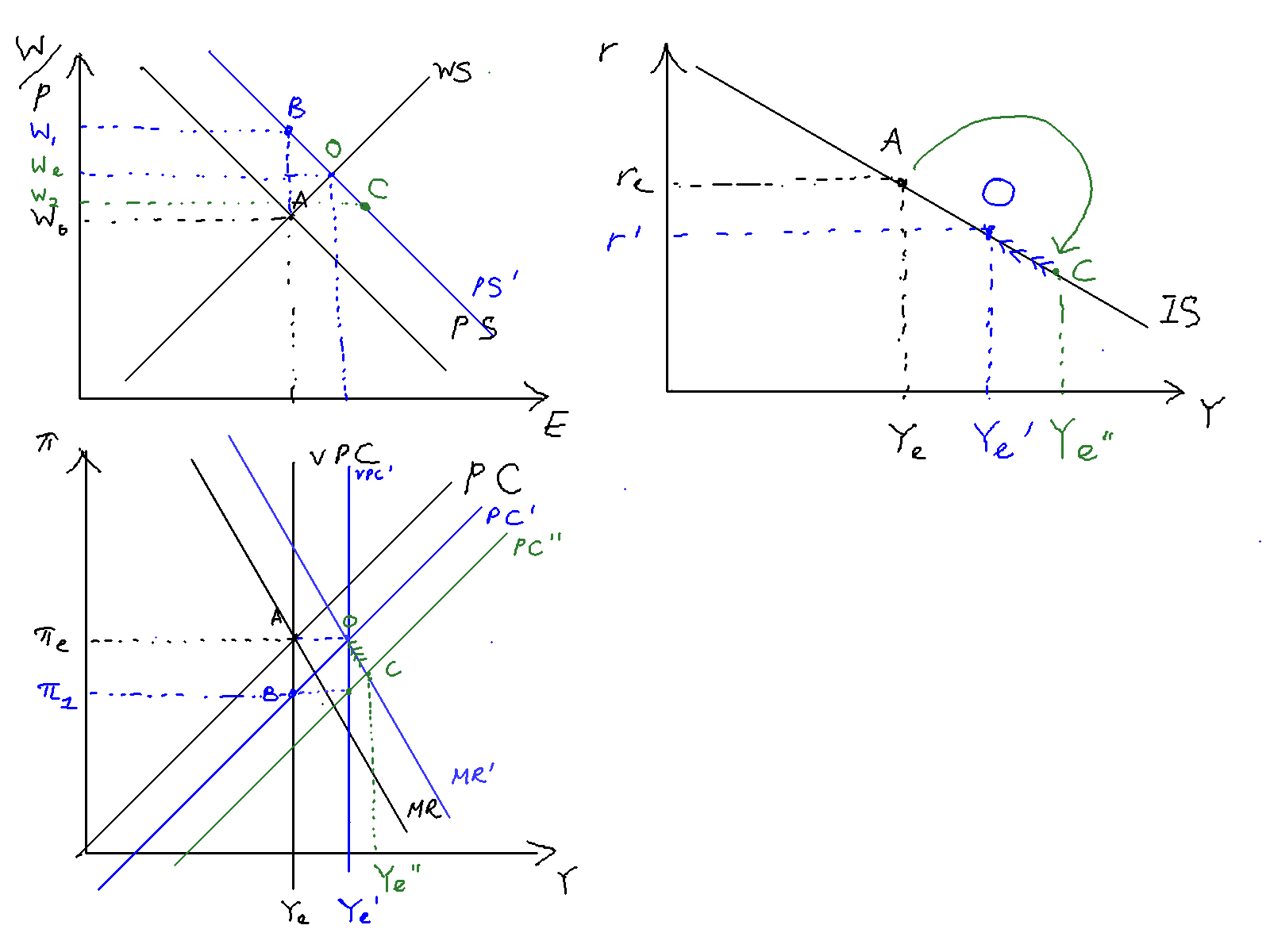

A permanent increase in worker productivity

Consider an unexpected and permanent increase in worker productivity in period as denoted in figure \ref{productivity_shock}.

An unexpected and permanent increase in worker productivity increases the MPL, which in turn shifts the PS right, from . As the VPC is defined as the intersection of the WS and PS curves, the VPC moves from , in blue. This causes the PC and MR to move as well, as they must intersect the VPC at equilibrium inflation .

This unexpected increase in productivity means that goods are cheaper than expected, which results in lower inflation, from . (point A to point B). The unexpected lower inflation causes real wages to rise, from (in blue). The level of involuntary unemployment also increases, because at this higher level of real wage there are more people who would like to be employed but are not.

The central bank forecasts that this will cause the AEPC to move from (blue to green) in the next period, and lowers interest rates to reach point C, the intersection of and . Because there is a one period lag in the effect of real interest rates on output, however, this does nothing this period.

In period , the economy moves to the new output , and the AEPC shifts down from , and as forecasted the central bank lowers rates to reach point on the PC curve. Because output is greater than equilibrium, real wages are depressed to , which in turn causes involuntary unemployment to decrease.

From period onwards, there is a slow adjustment from to . Inflation rates slowly return to target and real wages go to the new steady state .

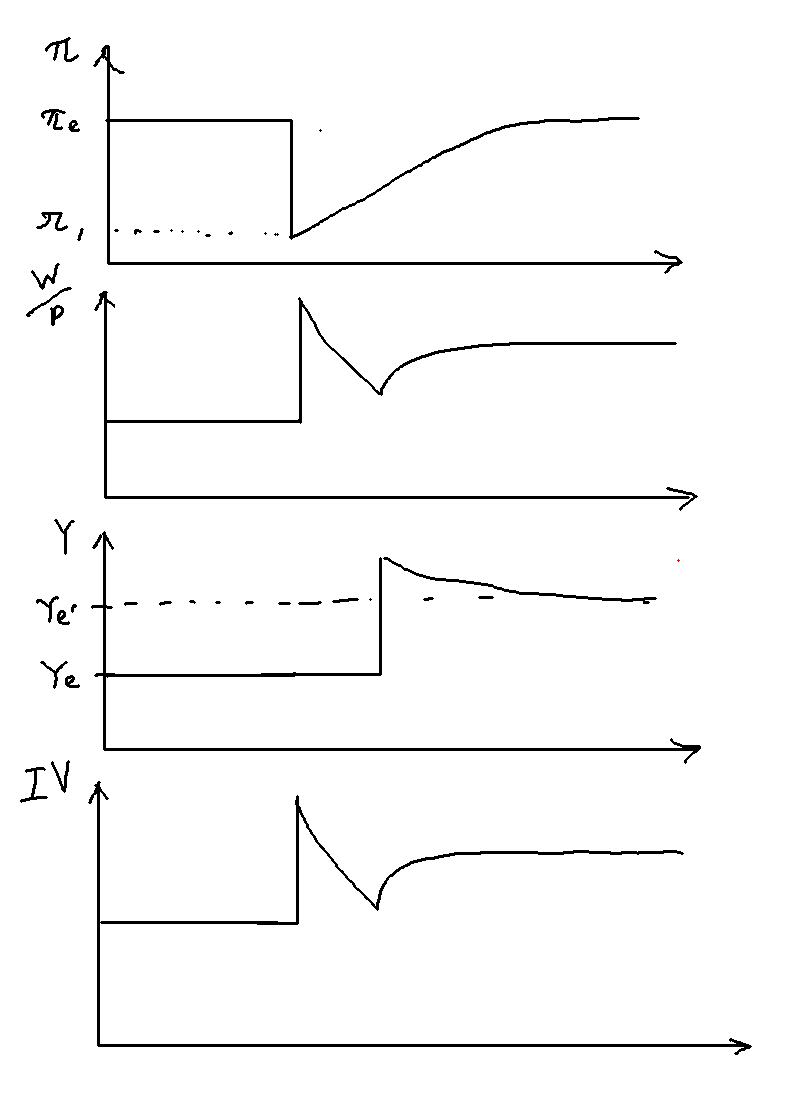

Figure \ref{prod_shock_adjustment_path} gives the adjustment paths for several key variables. In period 0, the time of the shock, inflation falls right away causing real wages to go up, which causes involuntary unemployment to go up. In period 1, output rises above equilibrium, causing real wages and involuntary unemployment to fall. In period 2 onwards, all variables slowly return to steady state.

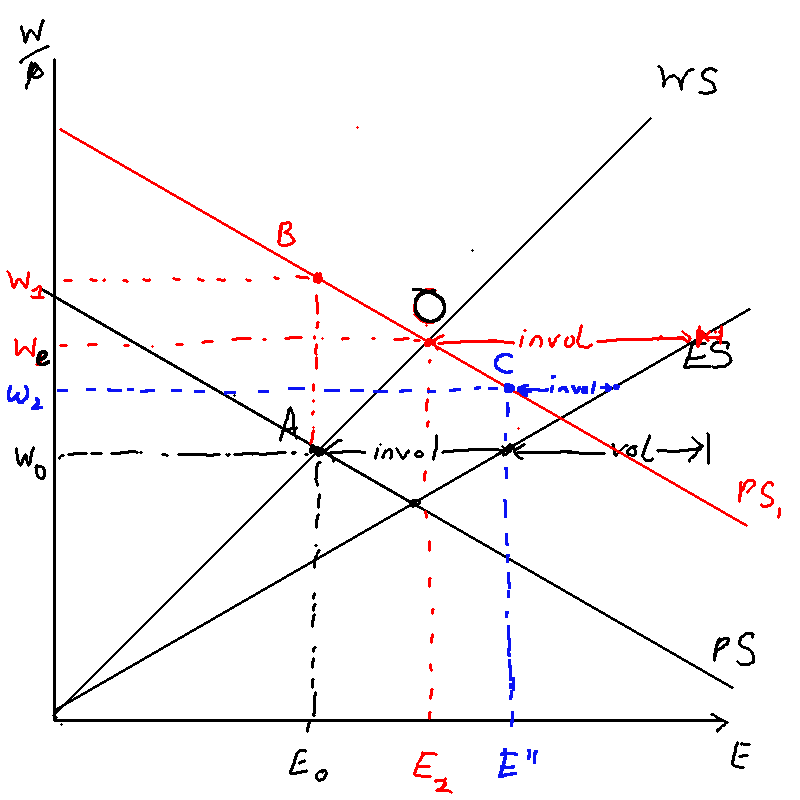

Whether involuntary unemployment increases or stays the same depends on the difference in the gradient between ES and PS. As Figure \ref{ps_shift} shows, involuntary unemployment shifts in period 1 as output is above equilibrium. But at the new steady state O, involuntary unemployment could be the same (if ES is parallel to WS) or it could be higher (if WS and ES diverge).

An unobserved change in worker productivity

[TODO]

In Chris Bowdler's slides.

A change in inflation target

A change in inflation target moves the MR.

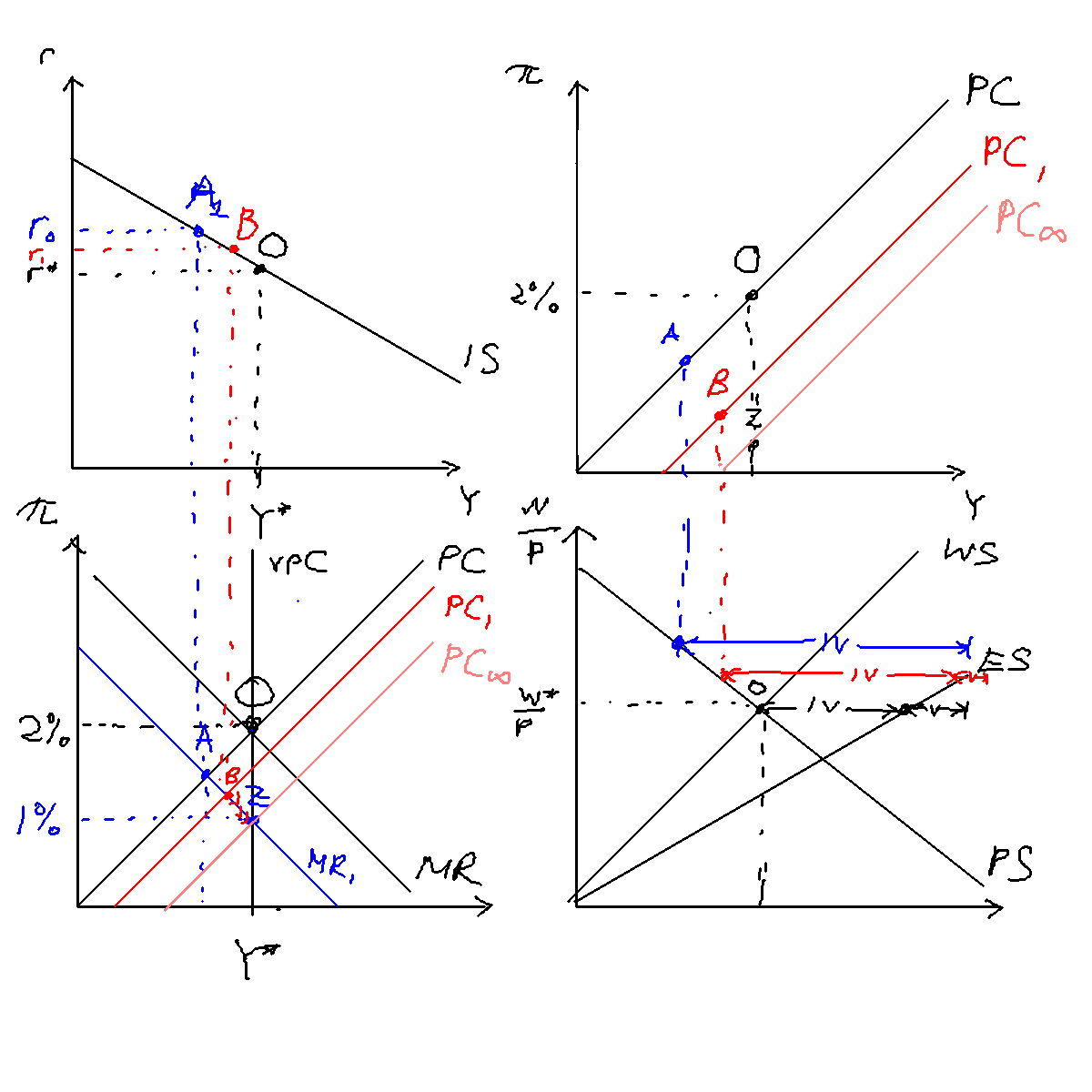

PYP 2016 Q2: A change in inflation target

- Consider the standard IS-PC-MR model presented by Carlin and Soskice in

which there is a one period lag in the effect of real interest rates on

output in the IS curve and the Phillips Curve is based on adaptive

expectations for inflation. Suppose that the inflation target is initially

2%. In period t the central bank decides to raise the inflation target to 4%

and its first opportunity to act on this new target is in setting real

interest rates in period t.

- Describe the process of adjustment for real interest rates, output and inflation from period t until the 4% inflation target is achieved.

- In period t+1, how does the deviation of the inflation rate from the 4% target depend on the slope of the Phillips Curve in output-inflation space? Explain the intuition behind your answer.

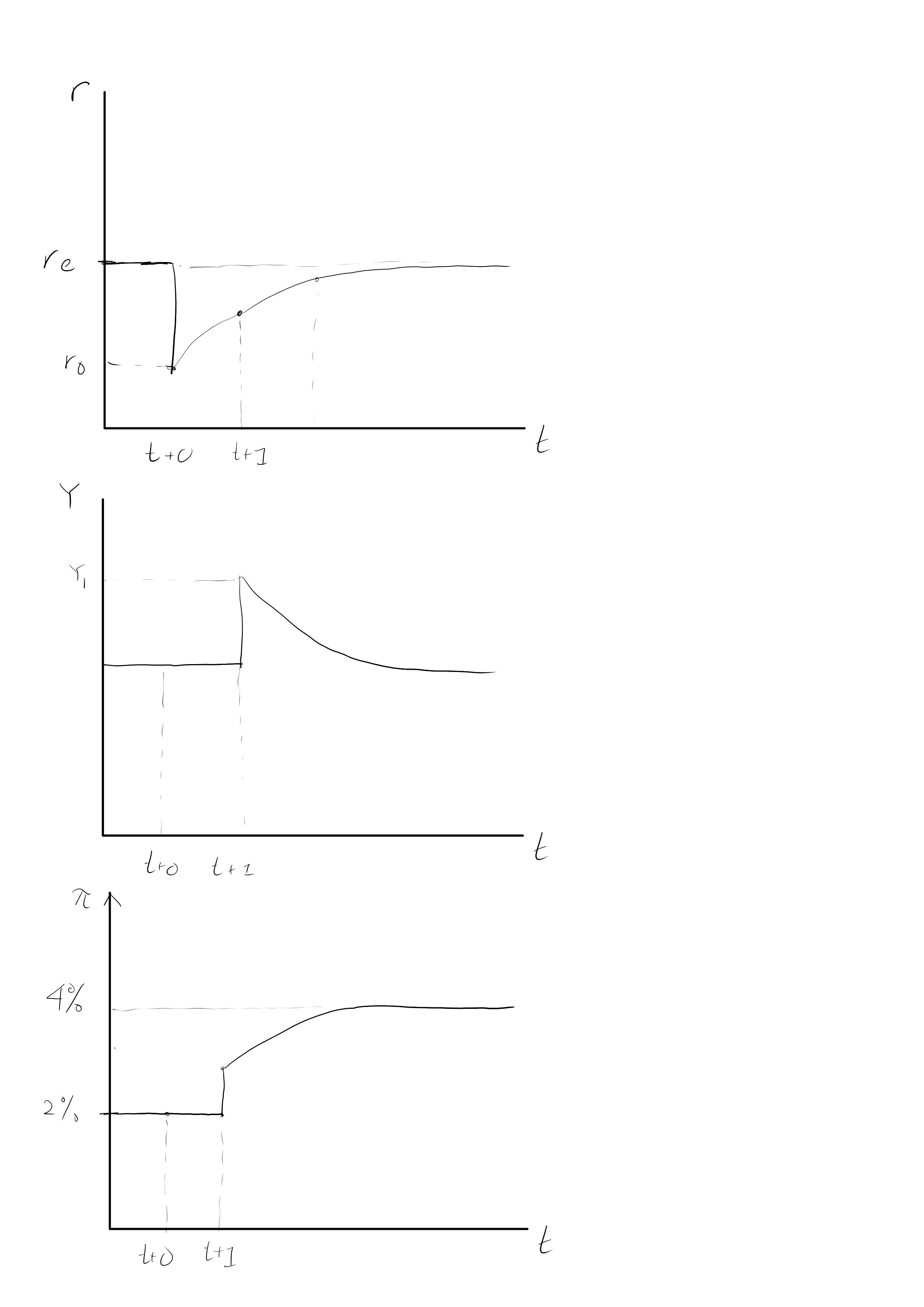

The economy is initially at equilibrium, with inflation at the target 2% and output at , where the VPC is. This corresponds to point O in the IS-PC-MR diagram. In period t, the central bank decides to raise the inflation target to 4%. This causes its MR curve to shift vertically upwards to intersect the VPC where inflation is 4%, at point Z. At this new MR curve (in blue), the central bank wants to locate itself on point A on . It thus lowers interest rates from to in period t. Because of the one period transmission lag between interest rates and output, however, nothing happens this period.

In period , the shock has had time to hit and inflation and output indeed rise, to the point A. The central bank forecasts that next period's PC curve will rise and thus raises interest rates to locate on the point B on the new PC curve (in red).

Henceforth, there is a slow adjustment of the economy---indicated by the red arrows---to the new equilibrium level of output and inflation, Z.

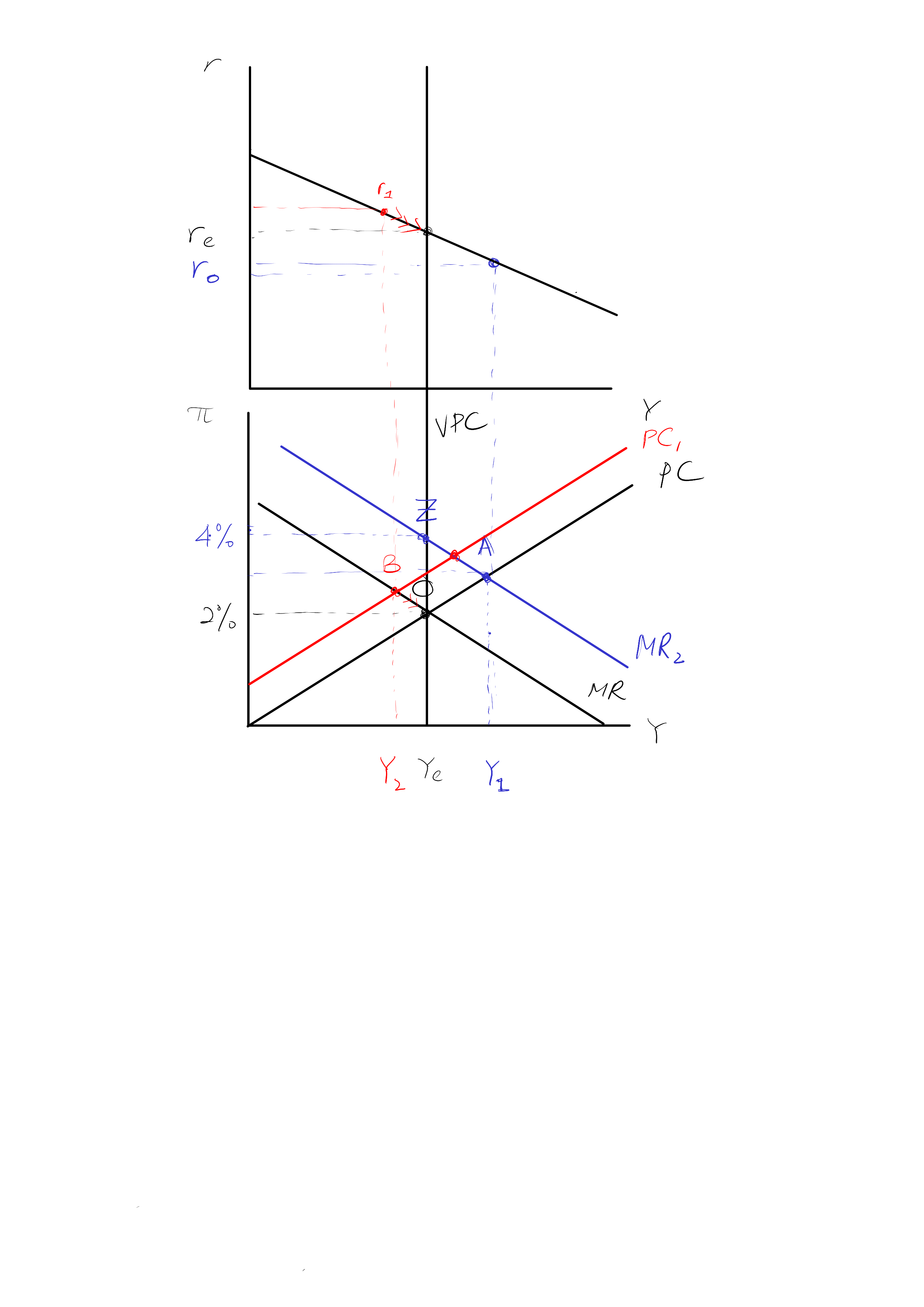

Now suppose that in period t+1 the central bank is advised that the new inflation target was a mistake and reverts to a 2% inflation target. The central bank sets real interest rates in t+1 based on the 2% inflation target.

- Describe the process of adjustment for real interest rates, output and inflation from period t+1 until the 2% inflation target is achieved.

- State a condition under which the central bank achieves inflation equal to the 2% target in period t+2 (continue to assume that inflation expectations are set adaptively).

In period , the bank again forecasts that the PC curve will shift upwards to and raises its interest rates to in order to locate on point B on .

In period , output and inflation fall, going to point B as forecasted, and there is a slow adjustment back to equilibrium henceforth.

The condition under which the central bank achieves inflation equal to the 2% target in period t+2 is if the central bank's MR curve is horizontal; that is, if in the MR equation

This represents a central bank that is so inflation-adverse as to be willing to raise interest rates infinitely to cut inflation immediately.

Dynamic loss functions

Previously central banks had a static loss function of

But of course central banks care also about the future,

Central banks now have a dynamic loss function of

where they care about future deviations more

The effect is to flatten the MR curve, because a central bank is willing to eat more losses now to have a smaller future stream of losses. In the degenerate case where (central bank has an infinite time horizon), the central bank's MR is essentially flat.

PYP 2017 Q5: does a dynamic loss function lower current interest rates?

"The more importance a policy-maker attaches to future inflation outcomes the lower the current inflation rate will be." Discuss.

On the face of it, the statement is obviously not true, because current inflation rate depends not just on the central bank's inflation target (which can be high or low, independent of how it views future outcomes), but also on unexpected supply shocks. For instance, a central bank which targets a 10% inflation and cares a lot about future inflation will have a higher inflation rate than a central bank that targets a 2% inflation but is more laissez-faire. Similarly, supply shocks like cost-push shocks or decreases in labour productivity can have the effect of pushing up current inflation, and due to the lag of interest rate transmission to output, current inflation can remain high despite the central bank's best efforts.

However, ceteris paribus, a central bank with a bliss level of output above equilibrium will generate less inflation bias with a dynamic loss function, compared to a static one.

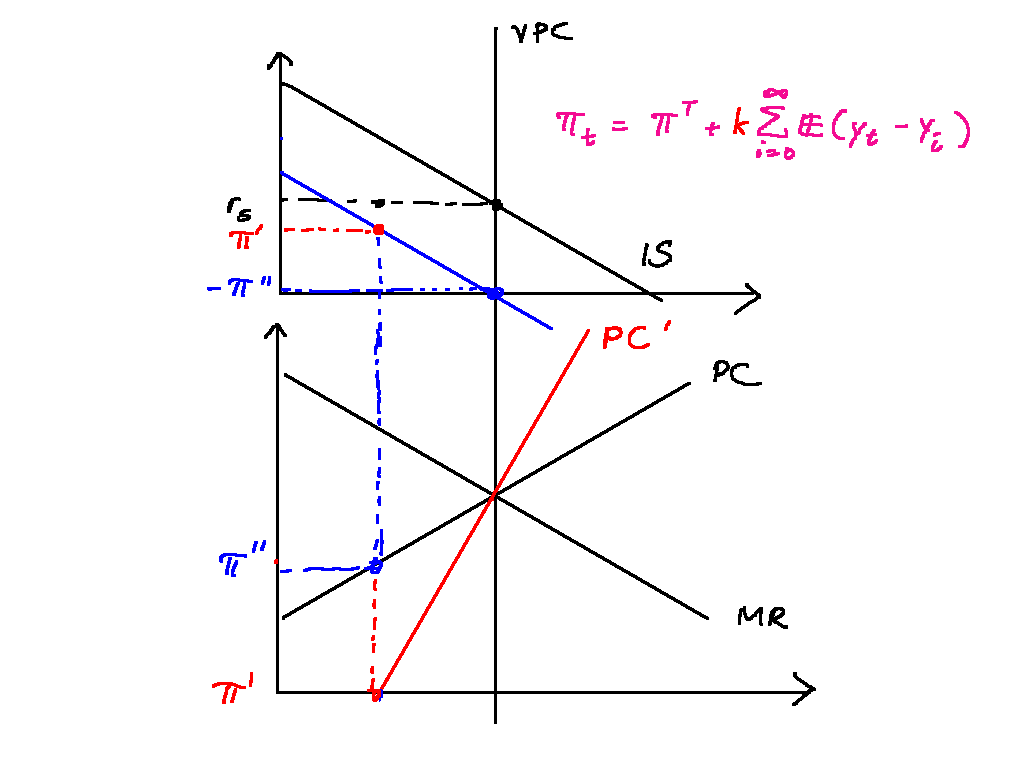

Let us first begin by setting up the model. The policy-maker/central bank has a target level of output and inflation , and has a quadratic loss function of

From this loss function, we can see that the central bank cares about deviations from output and inflation. The degree to which the central bank cares more about inflation is given by the parameter . The higher this parameter is, the more the central bank cares about inflation. At equilibrium, the current inflation rate will be equal to the central bank's target inflation rate, which can be high or low; thus the statement is not accurate.

We can construct the MR curve by taking the tangencies of the PCs with "iso-loss" curves given by the loss function. Figure \ref{pc_mr} shows how the MR is constructed.

Additionally, if central banks care about future inflation outcomes, then this means that they care about the infinite sum of future deviations from output and inflation, as follows:

I take the importance a policy-maker attaches to future inflation outcomes to mean the central bank's discount rate . The higher is, the less the central bank cares about future inflation: when , this reduces to the static loss function given earlier, and when , the central bank is infinitely forward-looking. While the MR always gives the central bank's best response in this period, we can think of the "effective MR curve" as the best response of the central bank taking into account future deviations that will result. The "effective MR curve" is flatter, because a central bank is willing to eat more losses now to have a smaller future stream of losses. In the degenerate case where (central bank has an infinite time horizon), the central bank's MR is essentially flat.

How does a flatter MR result in lower inflation? To do this, I introduce inflation bias. Consider a central bank with a target output above equlibrium, . This could be a welfare-maximising central bank, which is trying to reach the societally optimal level of employment where ES and MPL intersect. Or it could be more venal considerations like trying to impress the electorate.

Figure \ref{inflation_bias} shows how inflation bias occurs. While the equilibrium level of output is where the VPC intersects the PC at , the central bank has an output target . The economy starts off at with output at equilibrium and inflation at target, point A. However, at this point, the central bank wants io increase output to get to point B on the MR curve. Under adaptive expectations, However, this unexpected inflation will cause the PC to shift upward next period; the central bank's bliss point is now at C, and it decreases rates to reach that point. Again, this causes the PC to move up again.. This process repeats until point Z is reached, which lies on the central bank's MR.

Under rational expectations, society essentially reasons by backward induction. The central bank will best-respond to whatever belief they hold by moving onto the MR curve. The only rational belief in inflation is thus point Z. While the central bank would like to promise that it will remain at point A (which is a Pareto-improvement over point B), such a promise is not credible: if society did maintain inflation expectations at , the central bank would want to move to point B. This is called time inconsistency. Due to the time inconsistency problem under RE, the inflation bias problem is inescapable and more fundamental under RE than AE. While it seems plausible that society may play a grim trigger strategy (deviation triggers a permanent move to Z) to ensure central bank cooperation, this would fail renegotiation-proofness, and thus would not be a feasible equilibrium. Less grim triggers that trigger Z for a finite period can succeed in theory, but trigger strategies are normally thought to work well only in micro contexts in which the players might be two duopolists in a marker. Here player 1 is the central bank and 2 is the entire private sector covering millions for firms and workers and it is generally thought unrealistic that a decentralised private sector could coordinate the use of punishment strategies against the central bank.

Therefore, inflation that is permanently above output can happen when central banks have output targets above inflation. I now show how a central bank that cares more about future inflation outcomes will reduce this inflation bias. Consider the CB's dynamic loss function:

Consider the degenerate case . What is the central bank's best response at point A? The central bank deviates if and only if

While the central bank minimises its loss this period by deviating to point B, it knows that it would incur an infinite sum of greater losses in the future at point Z, which is further from its bliss point than point A is.

As such, it would not ever deviate: the effective MR curve is essentially flat, intersecting point A. Intermediate values of mean intermediate values of inflation bias. Figure \ref{inf_bias_dynamic} illustrates: a central bank with an intermediate value of would not deviate to B, because the future sum of losses incurred is too high. But if it deviates to , the future infinite sum of is not that much higher than the future infinite sum of , which is an attractive deviation.

While I have focused on the difference between a dynamic and static loss function (the future in "future inflation outcomes"), the central bank's own inflation aversion will also decrease inflation bias (the inflation in "future inflation outcomes"). A higher value in the central bank's loss function makes the isoloss curves more of an ellipse, which flattens the MR and thus reduces equilibrium inflation as previously analysed.

Rational expectations

People adjust their inflation expectations not according to last period's inflation expectations, but rather from predicted inflation, given all the information that they have at that point in time.

Here inflation today is formed by expectations of all information from the past that is available. means the expectation of from all information available at the end of period .

The key prediction of RE is that we essentially get costless disinflation! Consider a simple one-period demand shock, the same as before:

Under AEPC, people expect inflation next period to be (in blue). But this expectation would be thwarted as we know that the central bank would set rates to C, causing inflation expectations to actually be (in green). But if that's the case, then the central bank would set rates lower to go onto the MR line ... which would cause actual inflation to be even lower ... and thus the unique rational expectation would be .

This means that the after shock path is , with no central bank intervention needed!

Inflation bias

Inflation bias is caused by . This could be a welfare-maximising central bank, which is trying to reach the societally optimal level of employment where ES and MPL intersect. Or it could be more venal considerations like trying to impress the electorate.

There are three cases to consider:

- AE, static loss

- AE, dynamic loss

- RE, static or dynamic loss

Figure \ref{inflation_bias} shows how inflation bias occurs. While the equilibrium level of output is where the VPC intersects the PC at , the central bank has an output target . The economy starts off at with output at equilibrium and inflation at target, point A. However, at this point, the central bank wants io increase output to get to point B on the MR curve. However, this unexpected inflation will cause the PC to shift upward next period; the central bank's bliss point is now at C, and it decreases rates to reach that point. Again, this causes the PC to move up again.. This process repeats until point Z is reached, which lies on the central bank's MR.

In AE with dynamic loss the "effective" MR is flatter because the CB takes into account the future infinite series of losses so there is less inflation bias compared to the case with static loss.

Under RE, society essentially reasons by backward induction. The central bank will best-respond to whatever belief they hold by moving onto the MR curve. The only rational belief in inflation is thus point Z. While the central bank would like to promise that it will remain at point A (which is a Pareto-improvement over point B), such a promise is not credible: if society did maintain inflation expectations at , the central bank would want to move to point B. This is called time inconsistency. Due to the time inconsistency problem under RE, the inflation bias problem is inescapable and more fundamental under RE than AE.

Why don't society play a grim trigger strategy?

From Chris Bowdler:

If deviation triggers a permanent move to Z it is too grim and would fail the renegotiation-proofness requirement in game theory, i.e. one side would say to the other, deviation happened but that is now in the past, Z hurts us both so let’s renegotiate to A.

Less grim triggers based on deviation triggering Z for a finite period can succeed in theory given certain conditions on the discount rate and other model parameters are satisfied. But trigger strategies are normally thought to work well in micro contexts in which the players might be two duopolists in a marker. Here player 1 is the central bank and 2 is the entire private sector covering millions for firms and workers and it is generally thought unrealistic that a decentralised private sector could coordinate the use of punishment strategies against the central bank.

Countering inflation bias

- Independent central bank with closer to

- Independent central bank with lower discount rate

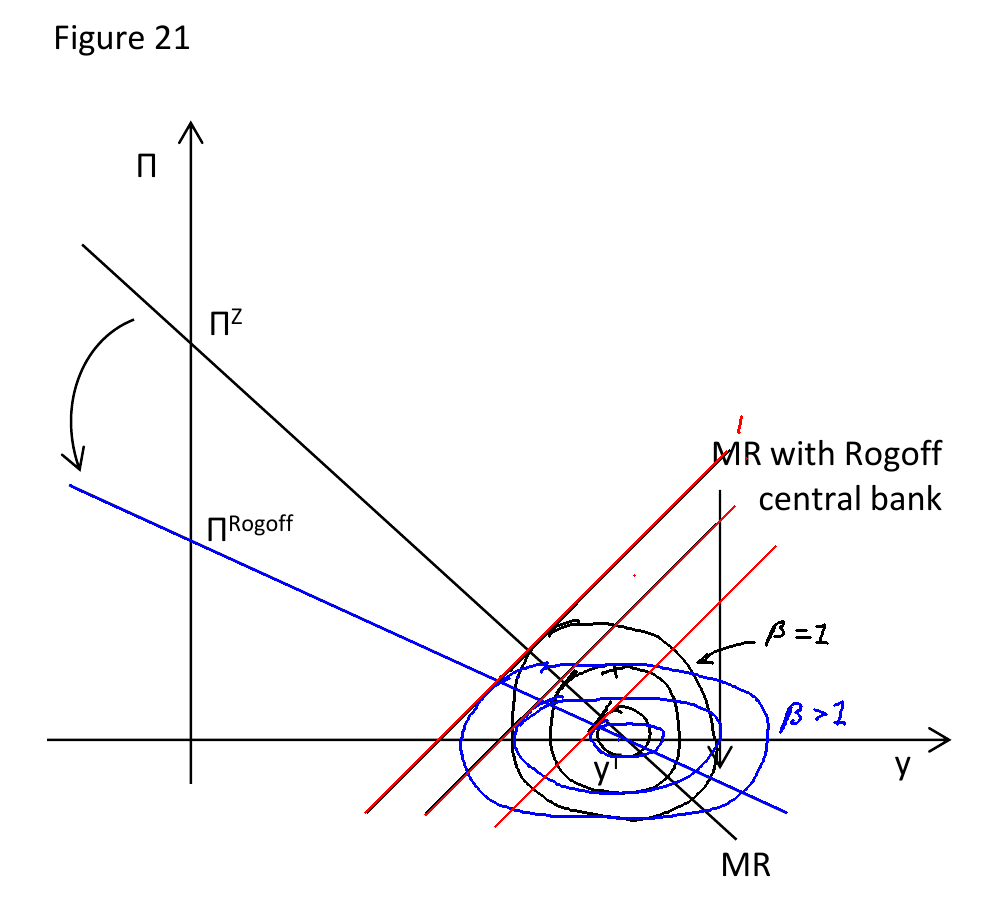

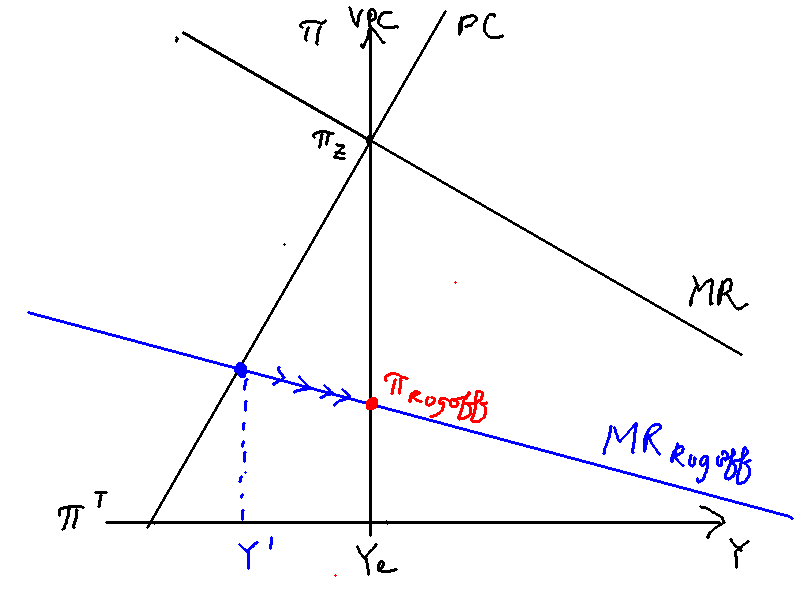

- Conservative central banker with low (Rogoff)

Most straightforwardly, one can delegate to a central bank with an output target closer to . If is closer to , then inflation bias will be reduced, as Figure \ref{cb_delegation} shows.

One can also delegate to an independent central bank with a longer time horizon (more patient discount rate). This has the effect of flattening the MR curve. As such, inflation bias will be reduced.

Lastly, one can delegate to a central bank which is more inflation-averse. As the MR takes the form

increasing the term flattens the MR curve. Figure \ref{rogoff_cb} illustrates. It draws the central bank's indifference curves for when and . As increases, the indifference curves become more elliptical, causing the MR to flatten.

Will the reform be welfare-improving? This depends on the discount factor of society. A myopic society will not want to appoint a conservative central banker. Assuming that society cares about both output and inflation, a conservative central banker will decrease output below equilibrium, which may be unpalatable to society. Figure \ref{rogoff_short_term} illustrates. Appointing a more conservative central banker increases , which has the effect of flattening the MR curve from to . The central bank will then raise rates to reach the point on its MR where output equals . There will then be a slow equilibration to , but the temporary fall in output may outweigh the permanently higher equilibrium inflation if society is myopic enough.

Sticky prices and monetary policy under the NKPC

Sticky prices

The problem with rational expectations is it gets us immediate and costless disinflation with no central bank intervention required, which does not accord with existing theory. Therefore, we introduce sticky prices.

Menu costs are the costs incurred from repricing goods, such as creating new barcodes and shelf labels or updating catalogues and websites, and will lead firms not to adjust their prices in response to demand shocks as long as the lost profit from non-optimal prices is not as great as the associated menu costs.

Intuitively, small menu costs do not appear large enough to account for the failure of prices to adjust when the economy is in recession and firms are facing losses. However Ball, Mankiw and Romer (BMR1988) present a model of staggered price setting whereby small menu costs lead to individually rational firms not adjusting prices due to "aggregate demand externalities" imposed on them by other firms.

Imperfectly competitive (since perfectly competitive firms are price-taking and have no choice but to vary prices after a demand shock) firms with rational expectations plan to reset prices at fixed intervals and the costs of these price adjustments are sunk. Prices can be adjusted between scheduled price reviews but only upon payment of a small menu cost.

If these menu costs were not present prices could adjust rapidly to clear markets after any shock; a negative aggregate demand shock would push down demand and marginal revenue curves faced by firms, leading all firms to reduce prices and reducing the aggregate price level. The falling price level would restore aggregate demand and firm output would revert back to the full employment level.

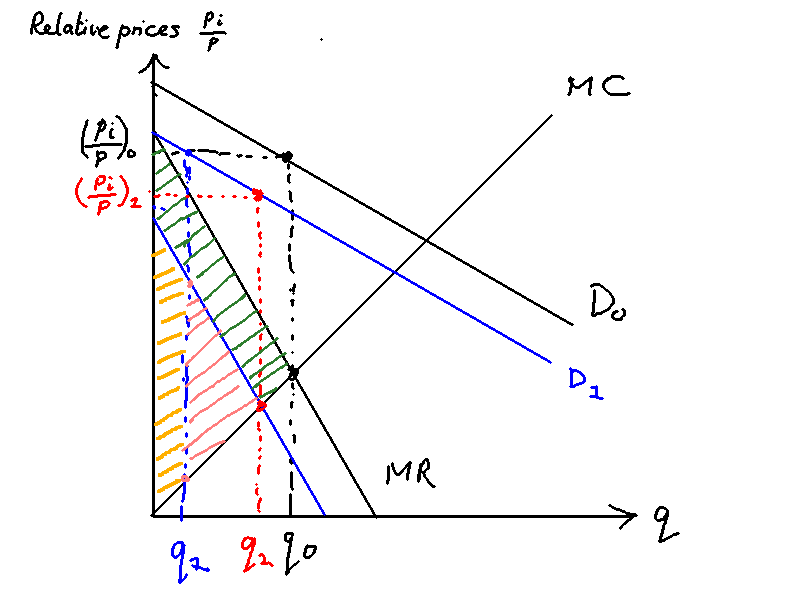

Things change when we introduce menu costs, however. Figure \ref{menu_costs} shows the marginal cost, revenue and average revenue (demand) of a representative firm . The firm originally faces a demand . As a profit-maximising firm with some market power it sets prices such that it sells the quantity where . It makes a profit of the area between the MR and the MC curves: that is the sum of the orange, pink and green areas.

Suppose now demand has fallen from to (in blue). A representative firm not undergoing a price review in the period when demand falls from to and marginal revenue shifts from to was previously setting real price at , where is relative price and the aggregate price level. If prices are not adjusted output falls from to . Its new profits are equal to only the orange area, resulting in a loss of profits due to inefficient pricing equal to the pink triangle and the green trapezium.

The firm would now prefer to adjust to . But the key here is that the firm will choose not to adjust prices whenever menu costs are greater than the pink triangle, not the sum of the pink triangle and the green trapezium. In other words, the profit that the firm can recoup by lowering its own price own price (pink triangle) is small relative to the loss of profits due to all other firms not adjusting prices and restoring aggregate demand (green trapezium).

So large losses to firm profits characteristic of recession may result from menu costs which are small relative to the scale of losses. Hence nominal rigidities have ‘aggregate demand externalities’; rigidity in firm prices due to menu costs can create rigidity in the price level which leads to fluctuations in real aggregate demand and employment.

When does price inertia happen?

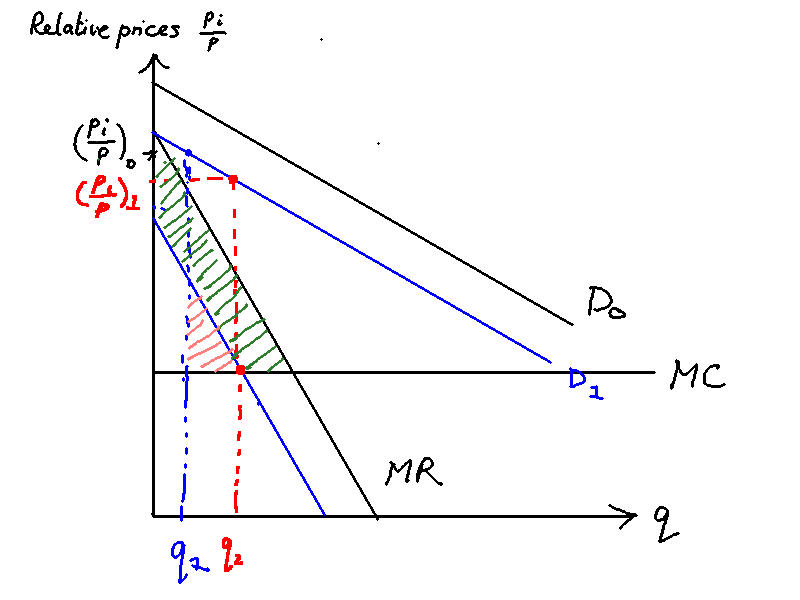

Price inertia is most likely to happen when the MC is flatter. Figure \ref{sticky_prices_flat_mc} shows a representative firm with a flatter MC compared to that in Figure \ref{menu_costs}. It can be seen that the area of the pink triangle is much smaller here. The marginal profit from raising output is smaller the flatter MC is. Hence the incentive is greater to stay at one's current output/price and avoid paying the menu cost.

Factors contributing to flat MC are known as real rigidities and include flat WS (since then labour costs vary little with employment and output)

Real rigidities can result in flatter marginal cost curves, for example through flat wage-setting curves which make labour costs relatively unresponsive to changes in employment and output. Hence these contextual factors exacerbate the effects of nominal rigidities such as menu costs.

A final factor affecting the adjustment of price levels is the existence of contracts in the labour market; firms do not hire labour from scratch in each period, but employ workers on formal contracts which legally prevent the adjustment of wages for a set period. Intuitively labour contracts may appear too short to create the kind of stickiness required for long periods of economic recession. However Romer (2006) describes the presence of ‘implicit’ contracts; many jobs involve firm-specific skills and attachments that outlast legal contracts, prompting workers to stay in their current roles as long as expected income-streams are not higher from outside opportunities. Since current wages may be relatively unimportant to this calculation, we should not expect wages to adjust to clear the labour market in each period.

Deriving the NKPC from menu costs

Now that we have the microfoundations of sticky prices, we can leave the justification aside and start building the NKPC (in effect operating on a higher level of abstraction).

We can simply handwave and say that at every period, a proportion of firms get to set prices costlessly, but have to pay a menu cost and they don't change their prices. This is Calvo pricing (1983).

When a firm sets its prices, therefore, it has to take into account the fact that it may not get to change its prices for many periods after that. The derivation in the slides[1] gives us

where

and is the proportion of firms who get to set prices costlessly.

Note that the NKPC depends on because the steeper the PC curve, the more the firms set prices that respond to output changes. This is a function of the WS-PS curves.

The interpretation of this NKPC is that current inflation today depends on expected future inflation and today's output gap. Expected future inflation is important because of sticky prices: firms take into account expected future inflation because they may not get to set prices in the future.

Compare with REPC:

where inflation today is formed by expectations of all information from the past that is available. means expectation of from all information available at the end of period .

There is also an equivalent formulation of the NKPC:

The interpretation of this NKPC is that current inflation is target inflation plus the sum of output gap today and all expected future output gaps. Again, the role for expected future output gaps comes from the fact that rational firms constrained by sticky prices must factor in the future impact of demand on inflation.

Contrasting the NKPC with the AEPC

The key difference between the NKPC and the AEPC is that people react instantly, and there's a "jump" in inflation once a shock hits. If the shock is protracted then inflation shoots up for one periods and slowly declines over time. For instance, take a look at the following NKPC:

If there is a persistent output shock that is known, then this will be encapsulated in the sum term: inflation today will increase by a large amount.

An anticipated demand shock under the NKPC vs the AEPC

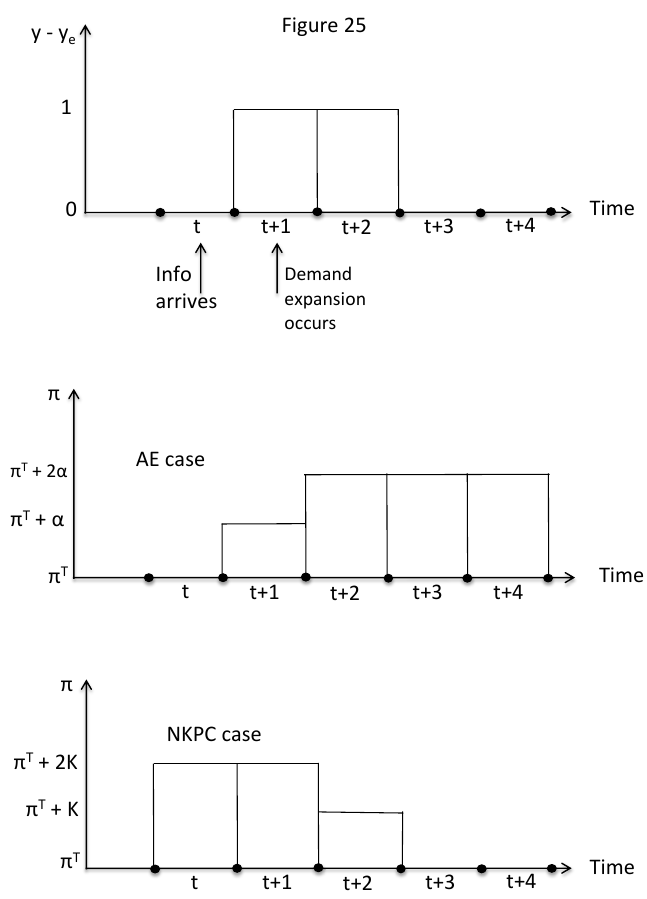

Figure \ref{nkpc_vs_aepc} illustrates the difference between the two PCs. For illustration, we consider a scenario where the central bank does nothing. There are two shocks forecasted in period that will come in period and .

Under the AEPC, nothing happens in period . In period the positive demand shock hits and inflation thus goes up to . In period the PC has shifted up, so expected inflation is , but the next shock hits causing inflation to go up again to , which causes inflation expectations to rise yet again. In the subsequent periods there are no longer any shocks, but inflation expectations remain elevated indefinitely until the central bank steps in.

Under the NKPC, forward-looking firms setting prices at time will take account of the subsequent demand shocks. Looking at the form of the equation, this will mean that inflation in period will be , as

In the same. In inflation falls to and in inflation returns to target. There is no intervention needed from the central bank.

This is quite counterintuitive, because empirical literature on inflation typically finds evidence of inflation persistence. In contrast, under NKPC inflation jumps around with no persistence whatsoever. Furthermore, a positive output gap in corresponds to a negative change in inflation, which goes against the common observation that periods of economic boom are times of rising inflation.

An unexpected demand shock under the NKPC vs the AEPC

Suppose we have two demand shocks happening at times and , both which are unexpected. Under the AEPC, there is no change. Under the NKPC, however, there is no change in time (because they don't expect it). In time , the shock arrives, causing inflation to go up to . In time , inflation expectations go back down, but there is yet another shock, so inflation stays put. Finally at time inflation goes back down to target.

A cost-push shock under the NKPC vs the AEPC

As with the AEPC, we augment the NKPC with a stochastic term:

Suppose there is a one-period unexpected positive cost-push shock, . What happens absent intervention by the CB? Simple: inflation goes up for one period and then goes back down again.

Similarly, what happens if the shock comes unexpectedly, but is known to last for two periods? Then inflation goes up to in the first period, in the second, and back to target in the third. There's a trend here: there is no need for central bank intervention, the economy will equilibrate itself, and there is no persistent.

Similar analyses obtain for permanent productivity shocks/demand shocks/etc.

Optimal monetary policy under the NKPC

Overall, while the NKPC combines microfoundations of rational expectation and sticky prices to give us a theoretically elegant model, the inflation dynamics that it predicts appear to be at odds with the inflation persistence and the positive correlation between output and inflation that are seen empirically in the data. When shocks are unexpected, results from NKPC are more in line with the data.

We've also seen that under NKPC (or indeed any sort of rational expectations framework), shocks correct themselves, what room is there for the central bank to intervene? It turns out that the central bank can send signals over future interest rate changes that can move the economy closer to the bliss point and attenuate output/inflation deviations.

We've seen that the NKPC incorporates future output deviations in determining inflation today:

This means that if the central bank can (credibly) signal that future output will be below equilibrium, it can in effect reduce inflation today. Here is an example: (I depart from Chris Bowdler's slides because he assumes that there is no lag in CB's actions and output --- but there's no need to, and one shouldn't, assume that).

Consider a one period unexpected positive cost-push shock that arrives at time , shown in Figure \ref{nkpc_stabilisation}. We know that the central bank doesn't have to do anything at all to stabilise this shock under the NKPC. In the next period the shock will disappear and we will get back to A. The path is thus : at time , at time , and again at time .

Is there room for central bank intervention? In fact, yes. The central bank can hike rates now for it to take effect in time . But given that it has hiked rates, inflation today will fall, as will decrease. We thus get the point . In , the NKPC goes back to normal, but the higher interest rates cause output to go below equilibrium, to point . Finally in the next period we return to equilibrium. We thus get .

Is this better? While the exact optimal monetary policy cannot be pinned down without doing the maths in full, the answer is yes due to the quadratic loss function: two small deviations are preferred to one big deviation.

Time-inconsistency of optimal monetary policy under NKPC

(The reason why CB chose to have there be no lag between the IS curve and the is so that you don't have to extend the analysis to two periods...)

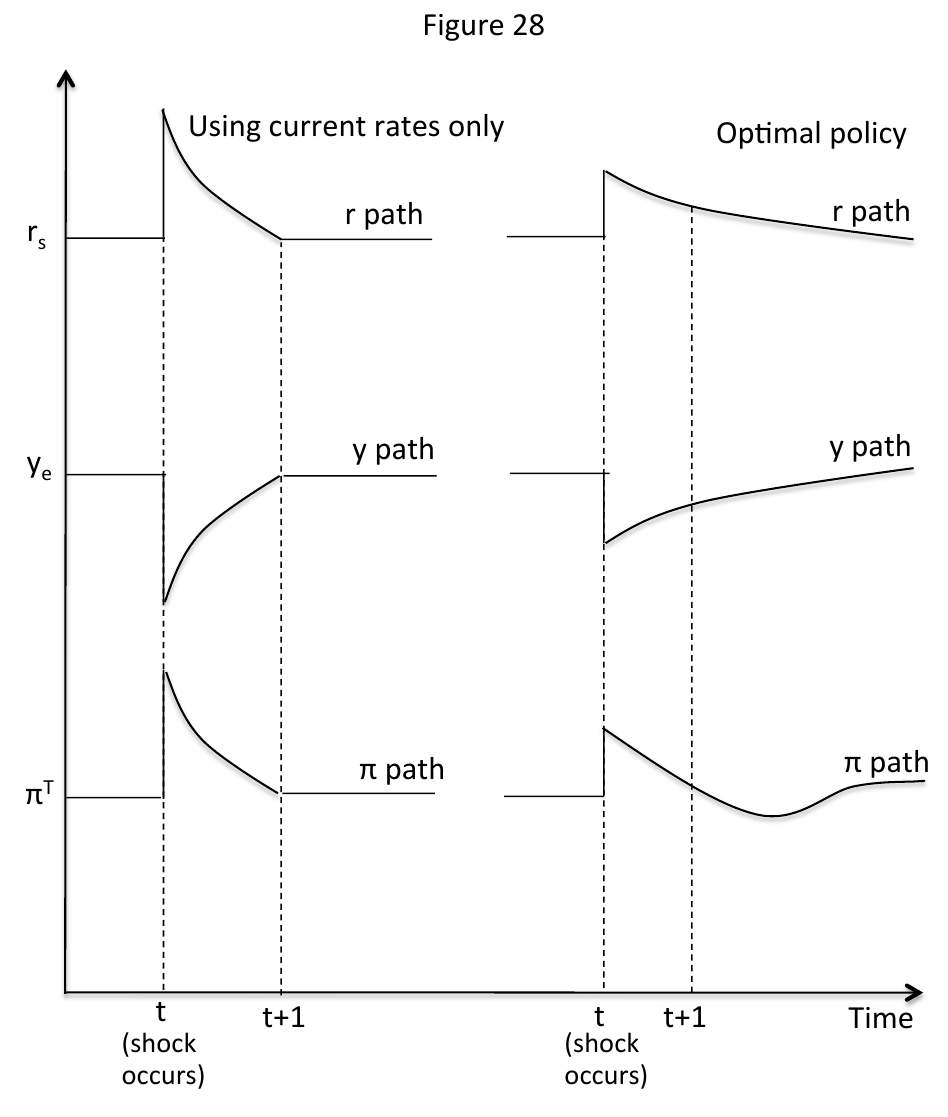

Suppose that the central bank would like to do even better by having a more protracted period of elevated interest rates. Figure \ref{nkpc_stabilisation_2} illustrates. If the central bank commits to two future periods of higher rates, then inflation today falls even further from to . The overall path is thus , which is better because it involves even smaller deviations than the previous.

The problem is that in period , the central bank has no incentive to raise rates to affect ! After all, we are already back at the original Philips curve, and the central bank's bliss point is at A. We thus have an issue of time-inconsistency: while the central bank would like to be believed---and indeed to be held to---a protracted rise in interest rates, such a strategy is not subgame perfect. Thus, no one will believe the central bank's proclamation in period that it will maintain rates for longer than the immediate future, which means that inflation will not fall as much as it could have if the central bank could issue a credible signal. This is stabilisation bias: the CB is forced to over-stabilise the economy through raising interest rates by more than is optimal because of its inability to commit to future interest rates.

Figure \ref{diff_paths} illustrates the result of stabilisation bias (in this diagram, there is no lag between interest rates and output). Because the central bank cannot use future rates to stabilise the economy, it must hike current rates higher, causing a sharp drop in output. Optimal policy flattens the curve: inflation doesn't spike as high during the shock because society expects a period of depressed future inflation.

Tackling the time-inconsistency problem with a price-path target

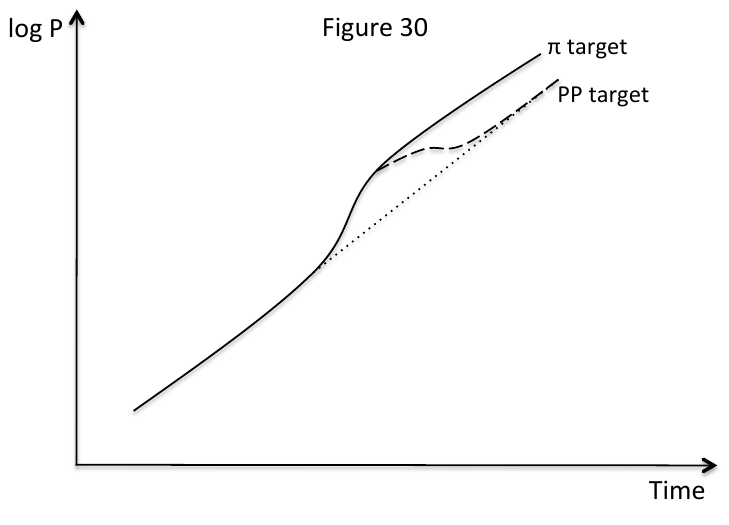

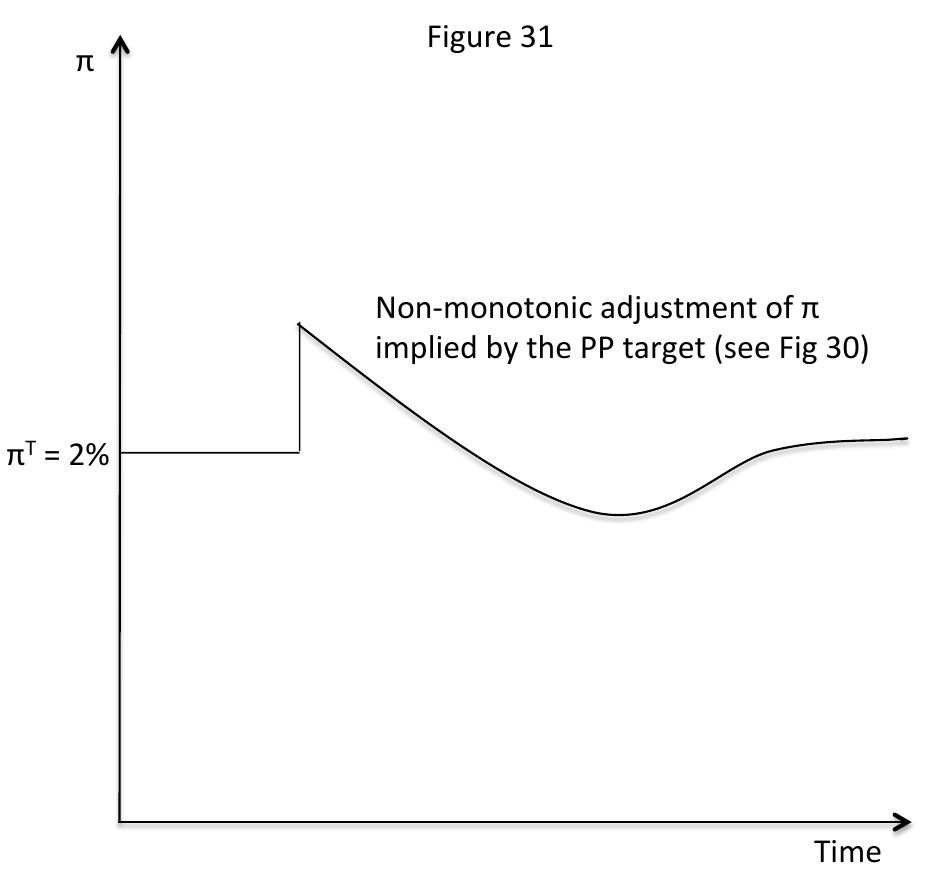

We have seen that stabilisation bias arises because the central bank is unable to credibly commit to lower inflation in the future. One way to tackle this is through what is known as price-path targeting. Inflation targeting targets a specific gradient of the price level, while price-path targeting targets a specific trajectory in the price level.

Figure \ref{pp_target} illustrates the difference between the two targets. The diagram depicts the log price level over time. When there are no shocks, price-path and inflation targets are identical. In the figure we introduce a positive shock. Inflation targeting cares about the gradient of the log price level and so adjusts it until the gradient goes back to normal, but price levels will be permanently higher than if there were no shock. Price-path targeting requires that the central bank raise rates and actually target a period of lower inflation in order to return to the previous price-path trajectory.

Figure \ref{pp_target_inflation} depicts the central bank's preferred inflation rate under price-path targeting. Observe that this diagram is very similar to the lower-right subfigure in Figure \ref{diff_path}! Under a price-path target, the central bank's incentives are aligned with the one in optimal policy, which means a credible future commitment, and greater macroeconomic stability.

The advantages and disadvantages of a price-path target

[TODO]

The key advantage of price-path target is that it renders the optimal policy time consistent. Recall that the central bank wants to credibly commit to higher rates in the future that cause inflation to be below target. But under an inflation target, once the shock dissipates, the central bank no longer wants to raise rates. A price-path target aligns these interests: the central bank wants to undershoot inflation in order to bring the price path back to its normal growth rate.

Additionally, a price-path target can be a remedy to the limitations of monetary policy at the zero lower bound. More on this later.

Rational expectations and sticky prices

[TODO]

A common exam question is: Will rational expectations make output and inflation more stable in the face of shocks?

2016 Essay: “The larger the share of private sector agents that hold rational expectations, the more stable output and inflation will be in the face of macroeconomic shocks.” Discuss.

2014 Essay: “The more rapidly inflation adjusts the shorter booms and recessions will be.” Discuss different circumstances in which this may or may not be true.

It depends on the model. Under RE, this is true. But under NKPC with sticky prices, this may not be true.

First talk about how rational expectations can give us costless disinflation under the REPC model.

Then talk about how

In fact, inflation may "jump" around under the NKPC model, making output and inflation even less stable.

In 2014 essay talk about just because inflation adjusts doesn't mean that booms and recessions may be shorter. For instance under the NKPC model, inflation adjusts but booms and recessions just as long. Or the central bank might intervene to make booms and recessions even more protracted (but milder). Less pronounced but more persistent movements in interest rates, output and inflation.

PYPs

2013 Essay: Why did rational expectations prove to be so problematic for traditional Keynesian theory? How did New Keynesian theory attempt to avoid these problems, and is this attempt empirically convincing?

Keynesian school of thought is that negative demand shocks cause recessions, and there is an active role for the policy maker to play.

New Keynesian theory attempts to avoid these problems by sticky prices: Calvo pricing backed up by Ball, Mankiw and Romer's (BMR1988) theory of menu costs. When all firms cut costs, all firms are better off: "aggregate demand externalities" on other firms, but firms don't do it because they can only control their private costs. Under this model, sticky prices prevail, and there is room for policymakers to stabilise.

As an example, take a negative demand shock that lasts two periods... (example). Under RE, expectations (and inflation) equilibrate right away without the CB having to intervene, but under NKPC inflation jumps and policymakers can reduce it by setting rates.

Is the attempt empirically convincing? It depends on whether or not you believe that menu costs are large enough to cause price rigidities, which depends on the shape of the MC curve among other things. Overall, not empirically convincing, because the NKPC adjustment path is opposite of what we expect (inflation correlates with output gap), and inflation persistence

2015 Part A: According to the New Keynesian Phillips curve, a one unit increase in the output gap relative to the previous period may be associated with either a rise in inflation relative to the previous period, no change in inflation relative to the previous period, or a decline in inflation relative to the previous period. Provide examples to illustrate each of these cases.

- An unexpected positive demand shock will cause an increase in output gap and inflation.

- No change: a shock that is known to last two periods arrives in time t, and we are now at time t+1 (the second period of the shock). Already priced in---no change in inflation.

- Decrease: a positive demand shock was supposed to be 2 units, but is in fact only 1 unit. Inflation decreases.

2015 Essay: Critically evaluate explanations for the existence of sticky prices in macroeconomic models. Would a greater degree of price flexibility have helped mitigate output losses during the recent Great Recession?

Question 8 (explanations for price stickiness and the impact of price flexibility on output during the Great Recession). This question was generally well answered. Most discussions of the foundations for price stickiness focussed on frictions such as menu costs, though only the best answers provided a full account of the role of the aggregate demand externality and real rigidities in ensuring that small menu costs would lead to aggregate price inertia. For the second part of the question weaker answers simply asserted that more price flexibility would help to return the economy to long-run equilibrium and so negate output losses. Stronger answers highlighted the role of the zero lower bound constraint during the Great Recession and discussed the ‘curse of flexibility’ whereby greater downward price flexibility would lower inflation and inflation expectations and so raise the real interest rate, potentially exacerbating output losses.

ADDED LATER: Should have mentioned that flexible prices means lower menu costs --> more likely to adjust --> goes to full rational expectations (costless disinflation)

Introduction

The existence of sticky prices starts with Ball, Mankiw and Romer's (1988) idea of menu costs and staggered price setting. This microfounds Calvo pricing (1983), which abstracts away this idea of menu costs by saying that firms can only revise their prices costlessly every so often.

Is this explanation a good one? This depends on the makeup of the economy: if marginal cost curves are relatively flat, then sticky prices are more likely to bite, as the marginal profit from a higher output is smaller the flatter MC is. Empirically, however, menu costs do not seem to be a good explanation for sticky prices: online storefronts with near-zero menu costs don't adjust their prices any more often than non-online stores.

Cavallo, Alberto. "Scraped data and sticky prices." Review of Economics and Statistics 100.1 (2018): 105-119. (evidence that online prices are not less sticky)

Finally, price flexibility would not have helped mitigate output losses during the recent Great Recession, and would in fact have made things worse: this is the so-called "curse of flexibility", where the economy falls into a deflationary spiral much more quickly if prices can adjust flexibly.

Why sticky prices exist

I first explain how sticky prices can arise from relatively small menu costs in the BMR model. Consider a market that contains imperfectly competitive (since perfectly competitive firms are price-taking and have no choice but to vary prices after a demand shock) firms with rational expectations plan to reset prices at fixed intervals and the costs of these price adjustments are sunk. Prices can be adjusted between scheduled price reviews but only upon payment of a small menu cost.

If these menu costs were not present prices could adjust rapidly to clear markets after any shock; a negative aggregate demand shock would push down demand and marginal revenue curves faced by firms, leading all firms to reduce prices and reducing the aggregate price level. The falling price level would restore aggregate demand and firm output would revert back to the full employment level.

Things change when we introduce menu costs, however. Figure \ref{menu_costs} shows the marginal cost, revenue and average revenue (demand) of a representative firm . A representative firm not undergoing a price review in the period when demand falls from to and marginal revenue shifts from to was previously setting real price at , where is relative price and the aggregate price level. The firm would now prefer to adjust to . If prices are not adjusted output falls from to , resulting in a loss of profits due to inefficient pricing equal to the triangular area shaded in pink. Call this area ABC.

The firm will choose not to adjust prices whenever menu costs are greater than the area ABC. The key observation however is that the loss of profits due to the firm being unable to adjust its own price (ABC) is small relative to the loss of profits due to all other firms not adjusting prices and restoring aggregate demand, denoted by the shaded green area. We thus have an explanation for how relatively small menu costs can result in sticky prices.

Is the BMR model a good explanation for sticky prices?

Is the BMR model a good explanation for sticky prices? That depends on the area ABC. If the area ABC is relatively large then small menu costs cannot adequately explain price inertia.

Price inertia is most likely to happen when the MC is flatter. Figure \ref{sticky_prices_flat_mc} shows a representative firm with a flatter MC compared to that in Figure \ref{menu_costs}. It can be seen that the area of the pink triangle ABC is much smaller here. The marginal profit from raising output is smaller the flatter MC is, hence the greater the incentive to stay at one's current output/price and avoid paying the menu cost. A flat marginal cost curve can be a property of the factors of production: for instance, flat wage-setting curves or labour contracts may make labour costs relatively unresponsive to price levels. In industries where marginal costs are relatively steep the BMR model will be a poor explanation of sticky prices. Empirically, moreover, online storefronts with low-to-zero menu costs do not change their prices any more often than brick-and-mortar storefronts: this suggests that there must be another explanation for sticky prices other than menu costs. Some have suggested that a lack of information is the culprit here: firms may not receive up-to-date information about demand levels, and thus (in a model akin to Calvo pricing) only update their prices when they receive that information.

How price flexibility could have exacerbated the Great Recession

I now set up the NKPC model of sticky prices to analyse a negative demand shock, showing how price flexibility would have increased the possibility of a deflationary spiral during the Great Recession. The NKPC derives from Calvo pricing, where in each period only a proportion of firms are allowed to change their prices. When setting their prices in this period, therefore, firms must consider not only the price level and output today, but also expected future output gaps. This gives us the following Phillips Curve equation:

The interpretation of the NKPC is as follows: current inflation is target inflation (because in the long run, the best estimate for inflation is that it will return to target) plus the sum of the output gap today and all expected future output gaps. Here where is the proportion of firms who get to set prices costlessly. We can see that more flexible prices are, the higher gets, and thus tends to .

We can now analyse the effects of price flexibility. The Great Recession can be modeled as a large negative demand shock --- so large that the zero lower bound (ZLB) bites. A large negative demand shock requires the central bank to set low real interest rates to raise output and inflation back to target. However, the zero lower bound means that nominal interest rates cannot be set much lower than zero, as companies and households have the option of holding cash. This means that the minimum interest rate that the central bank can set is . If the shock is large enough, however, this minimum real interest rate will not be low enough to bring output back to equilibrium. There will thus be a negative output gap in the next period. But the negative output gap in the next period then lowers inflation today to an even greater extent by the NKPC equation, which means that the minimum interest rate will rise, which will result in an even larger output gap... and so on. This is the deflationary spiral that can result from a large negative demand shock.

To counteract this, the central bank can issue guidance that it will keep policy rates low for a long period of time, which will decrease long-term rates. This has the effect of increasing demand for consumption and investment, which shifts the IS curve to the right. It can also purchase assets like government and corporate bonds to increase the money supply.

However, price flexibility during the Great Recession would have made the central bank's job harder. This is because price flexibility increases the slope of the PC: since

a higher proportion of agents who can set prices costlessly will increase k. The same demand shock will cause inflation today to fall to a greater degree, which will demand a greater response from the central bank.

Conclusion

In conclusion, the BMR model can explain sticky prices only if marginal cost curves are relatively steep and there are little real wage rigidities. Price flexibility means a steeper NKPC curve, which makes stabilisation more difficult because i) the ZLB is more easily reached and ii) once the ZLB is reached, the deflationary spiral is more vicious.

2018 Essay: “Under the assumptions of the New Keynesian Phillips Curve (NKPC) a policy-maker can achieve more efficient stabilization of output and inflation in the aftermath of macroeconomic shocks than under alternative versions of the Phillips Curve. However, this result is of little value to policy-makers given that the assumptions underpinning the NKPC are unlikely to hold in practice.” Discuss.

- What are the assumptions underpinning the NKPC? (rational agents, sticky prices). Explain why thay are likely to hold in practice.

- Talk about how the policymaker can achieve more efficient stabilisation under the NKPC using forward guidance.

- Talk about why the policymake can't actually due to time-inconsistency.

The reason why the result is of little value to policy makers is not that the assumptions underpinning the NKPC are unlikely to hold in practice, but rather because the central bank cannot credibly issue forward guidance that would make the NKPC better than the AEPC.

Compare the NKPC with the AEPC. How can a policy-maker achieve more efficient stabilisation of output and inflation? Consider a one-period demand shock under the AEPC vs the NKPC: they are actually the same. But under the NKPC the central bank can commit to higher rates in the future to decrease inflation expectations today and thus have a more prolonged, but more placid, adjustment path. But it can't credibly commit because such a policy is not time-consistent!

2016 Essay: rational expectations wrt output and inflation

6. "The larger the share of private sector agents that hold rational expectations, the more stable output and inflation will be in the face of macroeconomic shocks." Discuss.

The validity of this statement depends on one's specific model of rational expectations, and the definition of "stability" one uses. In this essay, I compare and contrast different models with one another in the face of a cost-push shock. I will first set up the adaptive expectations IS-PC-MR model and show how inflation and output respond to an unexpected cost-push shock. I then show how under a rational expectations model, there can be "costless disinflation" where output and inflation immediately equilibrate. I also show that in other rational expectation models like the NKPC model, with sticky prices, inflation can jump around equilibrium for a long period of time. Overall, therefore, the statement is not entirely true.

Moreover, this raises questions of what "stability" entails. Does stability mean a quick return back to equilibrium, or does it mean a small change in inflation in every period? A protracted period of inflation being above target or output below equilibrium may be considered more "stable" than having inflation fluctuate around rapidly, even if the latter reaches equilibrium quicker.

Consider an unexpected cost-push shock that arrives in period t=0. We augment the AEPC with a random variable .

In this case, = 1, and ; that is, inflation expectations always equal last period's inflation

Figure \ref{one_period_cost_push} explains. The economy is initially at equilibrium, with output = on the VPC and inflation at target. This is point O on the diagram.

An unexpected one-period cost-push shock in t=0 causes the PC to shift up to , in blue. Inflation rises from to . The central bank knows that the shock will dissipate in the next period. Under AE, however, inflation expectations will be permanently elevated (, causing the PC in period to be at despite the fact that the shock has dissipated. It therefore raises rates to to reach point B on the MR curve. However, because of the one period lag between interest rates and output, there is no change in this period.

In period t=1, the PC remains at as predicted, and we indeed move to point B on the MR. The central bank knows that this will cause the PC in the next period to fall, and again lowers rates to reach its preferred point on the intersection of the MR and the new PC (not pictured). There is therefore a slow fall in inflation and rise in output as the economy slowly returns to equilibrium.

What happens in the basic rational expectations model? In the REPC, inflation expectations don't blindly follow last period's inflation, but respond to all the information that is available.

When the shock hits in period t=0, the public knows that the central bank will want to raise rates to return to equilibrium. If the public sets inflation expectations to like in the AE case, then they would be mistaken as they would in fact be on point B on the curve. If this is the case, however, then the public would set inflation expectations equal to inflation at point B, . But at this level of inflation expectations, the central bank would again want to set rates to reach a lower inflation at point C (not pictured), which would mean the public wants to set inflation expectations even lower ... and so on. The only mutual best response is for inflation expectations to be exactly at point after the cost-push shock. Inflation thus jumps from to back to --- all without the central bank having to do anything! The same holds for when not all agents are rational: with a mix of AEPC and REPC agents, inflation will rise, but to a smaller extent than that predicted in the AEPC model.

This is the key idea behind the claim made in the question. Having all rational agents means an instantaneous transition to equilibrium, while a large proportion of rational agents means a smaller shock and a quicker adjustment to equilibrium.

However, this result only holds when there are no menu costs or "sticky information". I now show that in the NKPC with all rational agents, inflation and output can fluctuate around equilibrium just like in the AEPC case. In the NKPC, "menu costs" (BMR 1988) or "Calvo pricing" result in sticky prices. Firms do not constantly change their prices, which means that they set prices taking into account expected future output gaps:

Consider the same one period unexpected positive cost-push shock that arrives at time , shown in Figure \ref{nkpc_stabilisation}. In response, the central bank raises rates. There is a one-period gap between inflation and output, so there is no change in output this period. But given that it has hiked rates, inflation today will fall under the NKPC, as it is now common knowledge that output next period will decrease. decreases. We thus get the point .

In , the NKPC goes back to normal, but the higher interest rates cause output and inflation to go below equilibrium at point .

Finally in the next period we return to equilibrium. The adjustment path is thus .

Figure \ref{adjustment_path_inflation} summarises the adjustment paths of inflation under different models. The AEPC model has the largest shock and takes the longest to equilibriate, while the NKPC model has smaller fluctuations and equilibriates in two periods. Finally, the REPC model jumps out and back to equilibrium instantly. The same applies for output. Does that mean that rational expectation models are more stable? This hinges on the definition of stability. One might argue that the rapid fluctuations in rational expectations models (inflation acts as a "jump variable") could be thought of as instability. And while under the AEPC inflation and output are disequilibriated for a long period of time, the adjustment process is smooth and gradual.

Macroeconomics at the Zero Lower Bound

What is the ZLB?

The ZLB obtains because nominal interest rates cannot fall far below zero. Most central bank policy rates are rates in which the CB will lend short-term to commercial banks, but negative lending rates would expose CBs to losses which would be unsustainable and eventually undermine their independence (having to seek taxpayer bailouts). CBs also set deposit rates at which commercial banks can invest funds overnight, but again the outside option is to hold cash which offers a slightly negative return due to costs of storage/insurance. Therefore the CB's deposit rates also have a lower bound just below zero.

The ZLB is the lowest feasible real rate of inflation . If inflation expectations start at target, then because nominal rates cannot go much below zero.

How the ZLB can cause a deflationary spiral

(I believe that the ZLB can only cause a deflationary spiral in AEPC and REPC, not NKPC. Have sent an email to Chris Bowdler about it.)

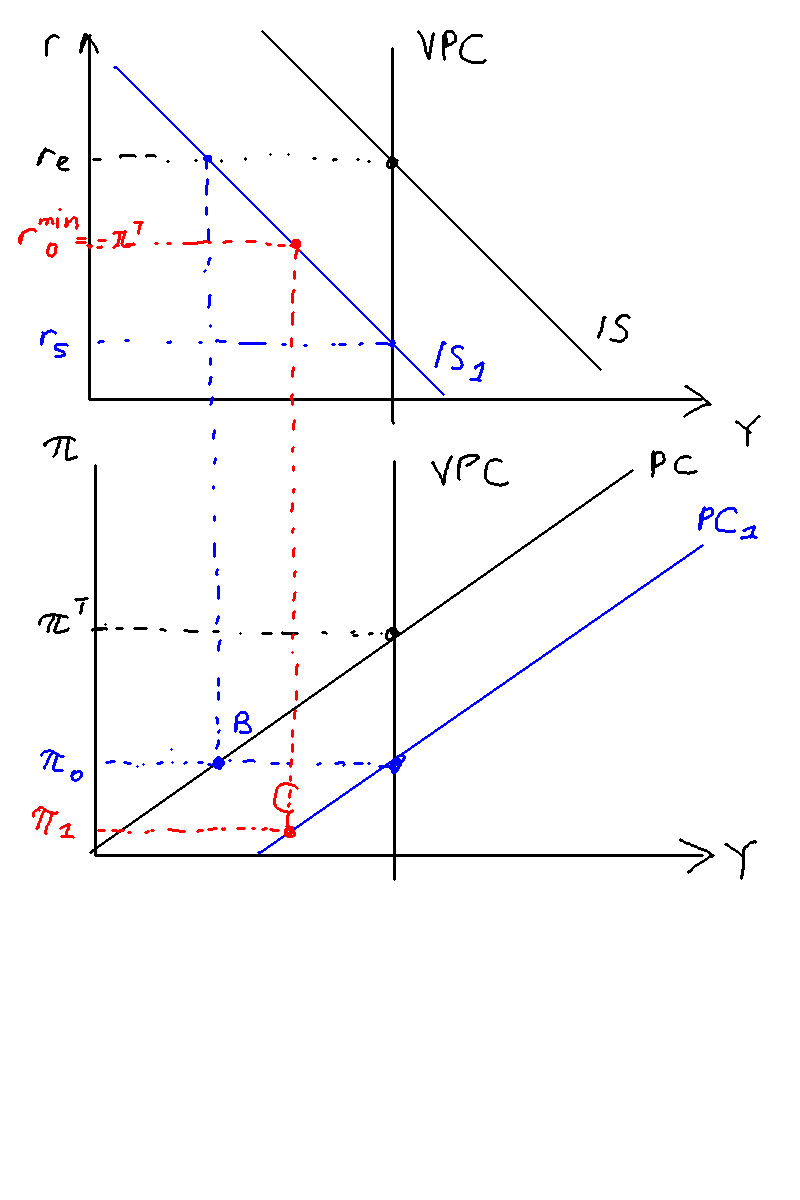

In Figures \ref{zlb1} and \ref{zlb2}, I lay out how a deflationary spiral occurs in the AEPC model. Start with Figure \ref{zlb1}. We have an economy at equilibrium at the point O, with inflation equal to target and output at the VPC. Now consider a huge negative demand shock that arrives at time . It is unexpected when it arrives, but it is known to last only for two periods. This causes the IS curve to shift left from from to (blue), which in turn causes output and inflation to fall from equilibrium O to the point B.

Because of the zero lower bound, the minimum real interest rate the central bank can set is , marked in red. However, due to the large magnitude of the demand shock, the real interest rate needed to stabilise the economy is actually lower, at . We will see what this means later. In any case, the bank sets the lowest rate it can which is in period , but it does not take effect this period.

At time , under adaptive expectations expected inflation is now at and thus the PC shifts from to , marked in blue. The rate the bank has set in period now takes effect, causing us to go to point C, marked in red.

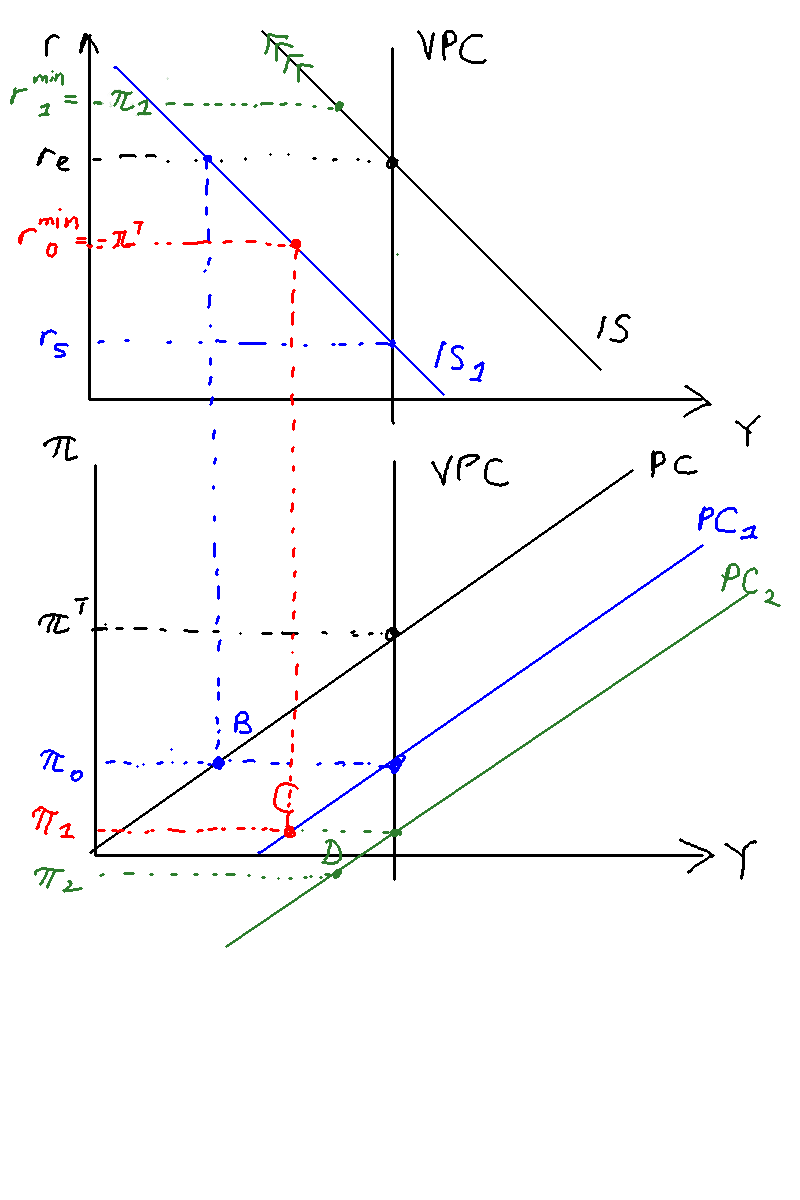

We now look at Figure \ref{zlb2} for what happens in period . At the end of period , the central bank wants to set interest rates as low as they can go. However, due to the disinflation in this period , the new minimum real interest rate is . So the central bank has no choice but to set that rate.

In period , the shock dissipates, and IS returns to normal. But it is too late. The rate that the CB has set is too high: inflation falls again to (point D, in green), which will cause next period to go even higher, forcing the central bank to set even higher rates... and so on. We thus get a deflationary spiral whereby the central bank moves higher and higher up the IS curve (denoted by the green arrows), and the PC just keeps falling and falling.

The crux is as follows: had the central bank been able to set the stabilisation rate in the first period , it would have been able to ride out the storm as it would lock down the PC and prevent it from falling further.

Under REPC, all this happens in an instant. Because the central bank cannot possibly stabilise the economy and all participants know this, we get an instant deflationary spiral all the way to negative infinity.

Furthermore, there is the possibility of hysteresis: equilibrium output may also adjust downwards as output decreases. For instance, unprofitable firms may suspend investment and allow depreciation to take effect, moving the PS left, or workers who have been unemployed for a long time may give up looking for jobs, moving the WS left. Both have the effect of moving to the left and end up inflicting permanent losses despite a very temporary demand shock.

Optimal policy at the ZLB

The central bank can issue time-dependent or state-dependent guidance that it will keep policy rates at the ZLB for a greater amount of time, which feeds into long term rates. While rates now may be at the ZLB, long-term rates may not be. How does this help? "Long rates matter for private consumption and investment because banks often source funding for mortgages and corporate loans in mooney markets in which the opportunity cost of money is the long-term government bond yield, so lower long rates mean cheaper financing for banks and ultimately for firms and households".

The IS curve we have drawn depends only on the real short rate, and so isn't able to capture this effect. But lower nominal and real long rates essentially shifts the IS curve to the right, because for the same short term rate and a lower long term rate, there will be more demand.

What if both short and long rates are at the ZLB? The central bank can commit to irresponsibility, pledging to keep rates at their ZLB not only until the economy equilibrates but until inflation exceeds the official target. In so doing, it raises the expected future inflation rate, which in turn lowers the real long term interest rate (as real rates = nominal rates - inflation). This doesn't suffer from the ZLB, as the central bank can commit to overshooting for as long as needed: future inflation can go up to positive infinity, meaning no lower bound on real long-term rates. We can thus push the IS curve as much to the right as needed to avoid the ZLB.

However, the bank again runs into the problem of time inconsistency. Once the economy equilibrates, the central bank has no reason to keep rates lower as promised. And thus this promise will not work in the first instance: rational agents don't believe the CB's commitment, meaning the ZLB problem cannot be overcome.

Price-path targeting allows the CB to commit to irresponsibility

Again, here PP targeting comes to the rescue! A PP target means that the central bank wants to commit to irresponsibility, because a large negative demand shock that results in a period of disinflation means that the central bank wants a period of high inflation to return to the original PP trajectory.

Another reason for a PP target is that it is symmetric: CBs under inflation targets often view their target asymmetrically. They are quick to snuff out but relatively lax about , letting inflation to equilibrate gradually. But this can lead to a demand deficit: if debt contracts are written on a 2% inflation assumption but average inflation < 2%, this amounts to a net wealth transfer from borrowsers to savers. The latter tend to have a lower consumption propensity and so overall demand drops, shifting the IS curve to the left and making it more likely to hit the ZLB.

"In theory extra saving generated should fund investment and correct problem, but credit market failures often mean this does not happen". A PP target forces the CB to behave symmetrically, preventing a lowered demand.

Concerns about price-path targeting

The main concern with PP targeting is that it does not work well with stagflation shocks. Consider a cost-push shock combined with a negative demand shock which causes inflation to go up. A PP target requires future inflation rates to go below equilibrium, which would imply expectations of real long rates today to rise, moving the IS curve to the left and exacerbating the recession. One response is to specify PP in a refined way that excludes stagflation drivers, but it's difficult to come up with a measure that works well in all circumstances. There are also control errors: more complex adjustment paths that are required by PP present a challenge to central banks, and correcting an inflation overshoot may drive inflation negative which would lead to a deflationary trap.

Also, committing to future inflation does not work with permanent supply shocks (shifts in the VPC) and may in fact exacerbate the problem. (why?)

Other ways of committing to irresponsibility

Quantitative easing: CB essentially "prints money" to purchase assets like government and corporate bonds, the CB essentially boosts the money supply. If QE is reversible (the CB can sell assets and unprint the money), but only slowly because a rapid sale of assets would lower prices and impose capital losses on CBs (but if it's printing money anyway, why should it care about losses???---because then it's giving free money to other people?), then this essentially locks the CB into higher future inflation since the CB cannot sell QE assets quickly enough to reduce the money supply. One possible interpretation of QE is thus a commitment technology for optimal monetary policy.

QE can also start lending directly to corporations and individuals. The commercial rate facing a borrower is